Volume

6, Number 3, 2019, R1–R57 journal homepage:

region.ersa.org

Volume

6, Number 3, 2019, R1–R57 journal homepage:

region.ersa.orgDOI: 10.18335/region.v6i3.267

REAT: A Regional Economic Analysis Toolbox for R

1 Karlsruhe Institute of Technology, Karlsruhe, Germany Received: 7 June 2019/Accepted: 4 November 2019Abstract. Methods of regional economic analysis are widely used in regional and urban economics as well as in economic geography. This paper introduces the REAT (Regional Economic Analysis Toolbox) package for the programming environment R, which provides a collection of mathematical regional analysis methods in a user-friendly way. The focus is on the identification of regional inequality, beta and sigma convergence, measurement of agglomerations, point-based measures of clustering and accessibility, as well as regional growth. The theoretical basics of the applications are briefly introduced, while the usage of the most important functions is presented and explained using real data.

1 Introduction

Methods of regional economic analysis (or regional analysis) are used frequently in theory-based, empirical studies from regional and urban economics as well as (quantitative) economic geography. These methods aim at analyzing some of the most important issues in the mentioned research fields, including (but not limited to) the existence and evolution of agglomerations, regional economic growth and regional disparities (Capello, Nijkamp, 2009; Dinc, 2015; Farhauer, Kröll, 2014; Schätzl, 2000). In any of the mentioned fields, a growing amount of quantitative data has to be processed when using traditional or novel methods and models of regional analysis. This paper introduces the package (add-on) REAT (Regional Economic Analysis Toolbox) (Wieland, 2019) for the programming environment R (R Core Team, 2018a). The package provides a collection of mathematical regional analysis applications, designed in a relatively user-friendly way.

The main topics in the regional analysis context can be summarized as follows, showing also the structure of the present paper with respect to the presented approaches and their application in REAT:

- Identifying regional inequality (or regional disparities) using indicators of concentration and/or dispersion (Section 2)

- Regional disparities over time leading to the concept of beta and sigma convergence (Section 3)

- Measuring agglomerations, which means the specialization of regions and the spatial concentration of industries as well as more complex cluster indices (Section 4)

- Point-based measures of clustering and accessibility (Section 5)

- Regional growth, especially shift-share analysis (Section 6)

Note that, in its original form, the open source software R is a command-line environment including a lot of mathematical and statistical features. For the installation of R and its packages as well as the basics of navigation and implemented statistical functions, see the R documentations (R Core Team, 2018b). A good supplement for working with R is RStudio (RStudio Team, 2016). The REAT package deals with several R data types: The most functions require and calculate numeric vectors, but, in some cases, also objects of type matrix, data frame and list, depending on the complexity of calculation. For a quick introduction to the data types in R and their properties, see e.g. Kabacoff (2017).

2 Concentration, dispersion and regional disparities

2.1 Indicators of concentration and dispersion

Regional disparities are a frequent topic in economic geography and regional economics. The spatial inequality with respect to e.g. regional output, income or employment is an essential element of polarization theory (Myrdal, 1957) and ”New Economic Geography” (Krugman, 1991; Fujita et al., 2001). Assessing regional disparities is possible using concentration and dispersion indicators, which belong to the univariate and descriptive analysis in statistics. Apart from regional economics, these measures are used in several contexts, such as competition economics (market concentration of firms) or welfare economics (income inequality). For a review of the most common indicators with respect to regional inequality, see Portnov, Felsenstein (2010), for studies comparing different indicators in the regional economic context using empirical data, see e.g. Gluschenko (2018); Habánik et al. (2013); Huang, Leung (2009); Palan (2017); Petrakos, Psycharis (2016).

Concentration is operationalized as the discrepancy between an empirical distribution of a variable x (e.g. annual turnover, income, gross domestic product [GDP]) with n observations or objects (e.g. competing firms, households, regions) and a (theoretical) equal distribution or a reference distribution (e.g. population distribution). Dispersion indicators aim at the deviation from the arithmetic mean of x, . In this context, Portnov, Felsenstein (2005, 2010) distinguish between measures of deprivation and variation.

Typical measures of regional disparities are the Gini coefficient, the Herfindahl-Hirschman index and the coefficient of variation (Lessmann, 2005). The most popular measure of concentration is the Gini coefficient (Gini, 1912) in combination with the Lorenz curve (Lorenz, 1905). There are several calculation approaches for the Gini coefficient, all producing the same result. The Lorenz curve is a graphical indicator, showing the deviation of the empirical shares of the regarded variable x from a (theoretical) equal distribution. Another well-known indicator is the Herfindahl-Hirschman index, which was developed independently by Hirschman (1945) and Herfindahl (1950), both in the context of competition economics. Several other concentration indicators are also applied in the fields of regional economics with respect to regional disparities, such as the Hoover coefficient (Hoover, 1936) and the Theil coefficient (Theil, 1967).

Except for the standard deviation, whose unit is equal to the unit of x, all common indicators are dimensionless. Most of them (except for standard deviation and coefficient of variation) have a fixed value range, normally between zero (indicating complete equality/dispersion) and one (indicating complete inequality/concentration).

Most of the common indicators are mathematically formulated in an unweighted and in a weighted form, while, in the context of regional disparities, the latter is mostly done using the regions’ proportion of the total (e.g. national) population (Doran, Jordan 2013; Lessmann 2014; Mussini 2017; Petrakos, Psycharis 2016; for a critical discussion of weighting these coefficients, see Gluschenko 2018). In the literature, there are different formulations where the weighted coefficients also include a weighted arithmetic mean. Note that, in the case of the population-weighted Gini coefficient, a weighted arithmetic mean is mandatory to keep the indicators’ value range.

Especially when dealing with GDP per capita as an indicator of regional economic output, several recent studies use dispersion measures rather than concentration measures, especially the (weighted) coefficient of variation (e.g. Lessmann 2005, 2014, 2016; Lessmann, Seidel 2017; Petrakos, Psycharis 2016). This dispersion indicator is a dimensionless normalization of the standard deviation. Weighting the coefficient of variation with population shares was introduced by Williamson (1965), which has led to calling this coefficient the Williamson index. As regional incomes or outputs are not normally distributed in most cases, resulting in biased arithmetic means used in the calculation of dispersion measures, the regarded variable may be log-transformed, which means replacing xi with log(xi) in the calculations.

Table 1 shows the common indicators, including their (population-)weighted and their normalized form (if there exist any) and the corresponding value ranges. The formulae are shown in a way that includes several ways of application. The regarded variable is always named xi, while the (population) weighting is called wi. Some indicators, such as the Hoover or the Coulter coefficient, require a variable representing a reference distribution the shares of xi are compared to. This reference is not a weighting. However, in many studies, the regional population is also used for the reference distribution. In these cases, reference and weighting are the same data. The reference distribution may also be equal to 1∕n.

Several indicators are also used for the analysis of regional specialization or the spatial concentration of industries, such as the Hoover coefficient or the Herfindahl-Hirschman index or its inverse (1∕HHI; also known as the “equivalent number” in the competition context). Other coefficients of concentration and specialization are discussed in Section 4. The last coefficient in Table 1, the mean square successive difference (von Neumann et al., 1941) is a measure for time variability not originating from but also transferable to regional economics.

| Indicator | Unweighted | Weighted | Normalized |

| Gini | G =  ∑

i=1n∑

j=1n ∑

i=1n∑

j=1n | Gw =  ∑

i=1n∑

j=1nw

iwj ∑

i=1n∑

j=1nw

iwj | G* =  G G |

0 ≤ G ≤ 1 - | 0 ≤ G ≤ 1 - | 0 ≤ G*≤ 1 | |

| HHI | HHI = ∑

i=1n( )2 )2 | HHI* =  |

|

≤ HHI ≤ 1 ≤ HHI ≤ 1 | 0 ≤ HHI*≤ 1 | ||

| Hoover | HC = | HCw = | |

[∑

i=1n| [∑

i=1n| - - |] |] |  [∑

i=1nw

i| [∑

i=1nw

i| - - |] |] | ||

| 0 ≤ HC ≤ 1 | 0 ≤ HC ≤ 1 | ||

| Theil | TC =  ∑

i=1n ln( ∑

i=1n ln( ) ) | TCw =  ∑

i=1nw

i ln( ∑

i=1nw

i ln( ) ) | |

| 0 ≤ TC ≤ 1 | 0 ≤ TCw ≤ 1 | ||

| Coulter | CC = | ||

![∘ 1-∑n-------xi------ri--2-

2[ i=1wi(∑ni=1xi - ∑ni=1ri)]](26725x.png) | |||

| 0 ≤ CC ≤ 1 | |||

| Atkinson | AI = 1 - [ ∑

i=1nx

i1-ϵ] ∑

i=1nx

i1-ϵ]

| ||

| 0 ≤ AI ≤ 1 | |||

| Dalton | δ =  | ||

| 0 ≤ δ ≤∞ | |||

| SD | s =  | sw =  | see CV |

| 0 ≤ s ≤∞ | 0 ≤ s ≤∞ | ||

| CV | v =   | see Williamson | v* =  |

| 0 ≤ v ≤∞ | 0 ≤ v*≤ 1 | ||

| Williamson | WI =   | ||

| 0 ≤ v ≤∞ | |||

| MSSD | MSSD =  | ||

Notes: xi is the i-th observation of the regarded variable x (e.g. GDP [per capita] in region i), xj is the value of the same variable with respect to object j, ri is the i-th observation of a reference variable (e.g. population), n is the number of objects (e.g. regions), is the arithmetic mean of x: =

∑

i=1nx

i, w is the weighted arithmetic mean

of x: w =

∑

i=1nx

i, w is the weighted arithmetic mean

of x: w =  ∑

i=1nw

ixi, wi and wj are the population weightings: Pi∕∑

i=1nP

i and Pj∕∑

j=1nP

j, where Pi

and Pj are the population sizes of regions i and j, respectively, ϵ is an inequality aversion parameter

(0 < ϵ < ∞) for the Atkinson index, t is a given time period and T is the number all regarded time

periods.

∑

i=1nw

ixi, wi and wj are the population weightings: Pi∕∑

i=1nP

i and Pj∕∑

j=1nP

j, where Pi

and Pj are the population sizes of regions i and j, respectively, ϵ is an inequality aversion parameter

(0 < ϵ < ∞) for the Atkinson index, t is a given time period and T is the number all regarded time

periods.

Compiled from: Charles-Coll (2011); Cracau, Durán Lima (2016); Damgaard, Weiner (2000); Gluschenko (2018); Heinemann (2008); Kohn, Öztürk (2013); Portnov, Felsenstein (2005, 2010); Taylor, Cihon (2004); Schätzl (2000); Störmann (2009)

2.2 Application in REAT

2.2.1 REAT functions for concentration and dispersion indicators

Table 2 shows the functions for concentration and dispersion measures implemented in the REAT package. All functions require at least one argument, a numeric vector with a length equal to n, containing the regarded variable x (e.g. income) with i observations (e.g. regions), where i = 1,...,n. This data may be a single vector or a column of a data frame or matrix.

An optional weighting of the vector x can be done using the function argument weighting which is also a numeric vector of length n. By default, the functions remove missing (NA) values. The hoover() function always needs a reference distribution (see the Hoover coefficient formula in Table 1), which is stated via the ref argument, also requiring a numeric vector of length n. If no reference variable is stated (ref = NULL), the reference is set to 1∕n.

All functions (except for disp()) return the single value of the computed coefficient. In the relevant cases (gini(), gini2(), herf() and cv()), a normalization of the coefficient is possible using the function argument coefnorm = TRUE, returning the normalized coefficient instead of the raw coefficient. The function disp() is a wrapper for all mentioned functions, calculating all coefficients (except for the MSSD) at once for one vector x or a set of variables/columns from a data frame or matrix.

Note that there are two functions for the Gini coefficient, gini() and gini2(), both producing the same result in the unweighted case. The former function is designed for income inequality, where the weighting option is designed for the calculation of the Gini coefficient for groups (e.g. income classes), where the weighting represents the group mean. The function gini2() is designed for the population-weighted analysis of regional inequality.

| Indicator | REAT function | Mandatory arguments | Optional arguments | Output |

| Gini/ | gini() | vector x | weighting vector, | value: G or G* |

| Lorenz | remove NAs, | or Gw, | ||

| Lorenz curve, | optional: plot (LC) | |||

| normalization | ||||

| gini2() | vector x | weighting vector Pi, | value: G or G* | |

| remove NAs, | or Gw, | |||

| normalization | ||||

| lorenz() | vector x | weighting vector, | plot LC, | |

| remove NAs, | value: G or Gw | |||

| and/or G* | ||||

| HHI | herf() | vector x | remove NAs, | value: HHI or |

| normalization | HHI* or NHHI | |||

| Hoover | hoover() | vector x | weighting vector Pi, | value: HC or HCw |

| reference vector ri | remove NAs | |||

| Theil | theil() | vector x | weighting vector Pi, | value: TC or TCw |

| remove NAs | ||||

| Coulter | coulter() | vector x | weighting vector Pi, | value: CC |

| remove NAs | ||||

| Atkinson | atkinson() | vector x | remove NAs, | value: AI |

| epsilon | ||||

| Dalton | dalton() | vector x | remove NAs | value: δ |

| SD | sd2() | vector x | weighting vector, | value: s or sW |

| remove NAs, | ||||

| treating as sample | ||||

| CV | cv() | vector x | weighting vector, | value: v or vW |

| remove NAs, | or v* | |||

| normalization, | ||||

| treating as sample | ||||

| Williamson | williamson() | vector x, | remove NAs | value: WI |

| weighting | ||||

| vector Pi | ||||

| MSSD | mssd() | vector x | remove NAs | value: MSSD |

| All indicators | disp() | vector x | weighting vector Pi, | matrix with 13 |

| or vectors x1,x2,... | remove NAs | (no weighting) | ||

| from dataframe | or 19 indicators | |||

| (incl. weighted) | ||||

Source: own compilation.

2.2.2 Application example: Small-scale regional disparities in health care provision

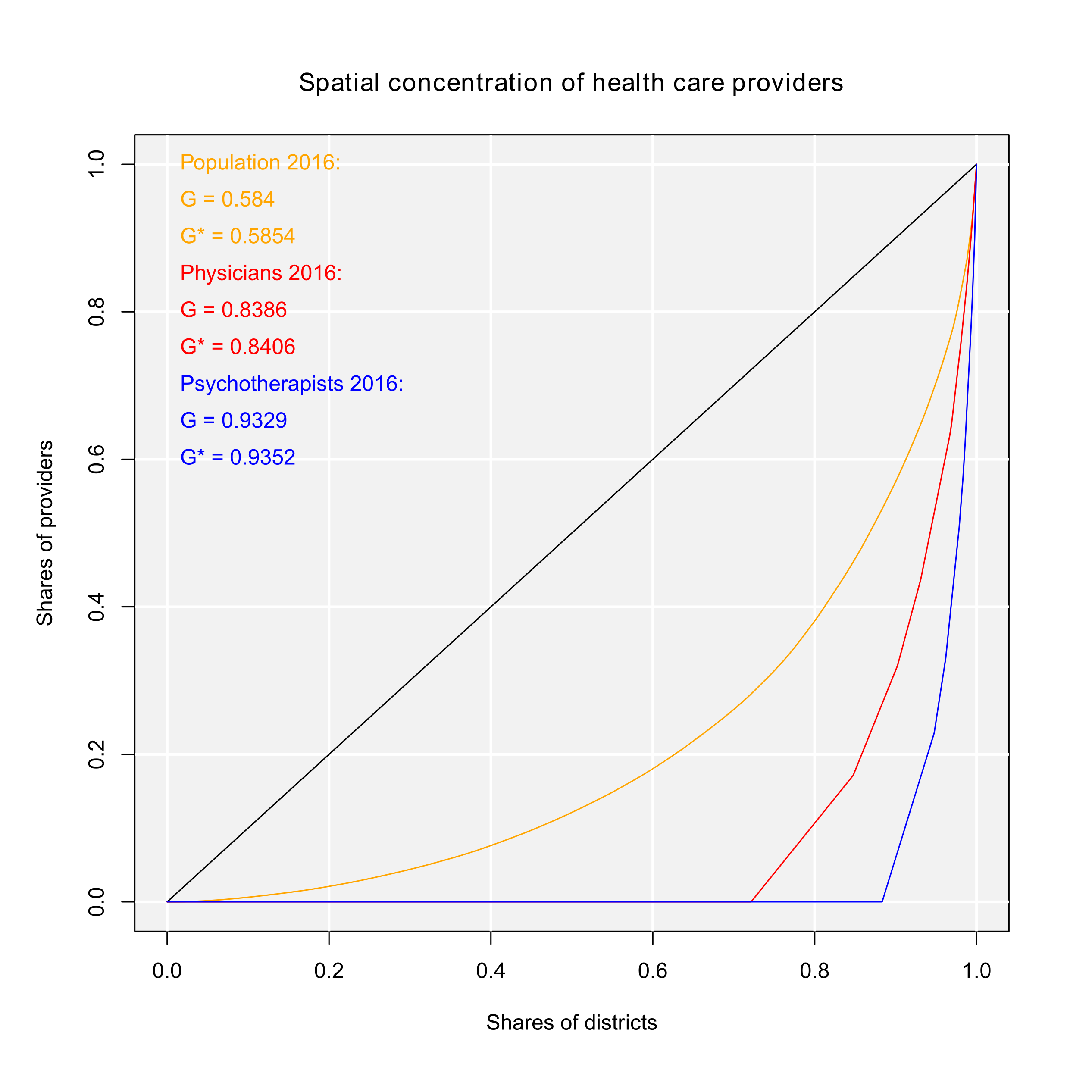

Regional inequality with respect to health care providers is a topic of high societal significance. In Germany, the health care planning system (Kassenärztliche Bedarfsplanung) attempts to flatten the disparities of local health care provision (Kassenärztliche Bundesvereinigung, 2013). Here, we analyze small-scale regional disparities in health care provision in two neighboring German counties (Göttingen and Northeim) using the data on medical practices and local population from Wieland, Dittrich (2016). The data is stored in the datasets GoettingenHealth1 and GoettingenHealth2, both included as example datasets in the REAT package. The study area is segmented into 420 districts, representing either city districts of larger cities or villages and hamlets.

The dataset GoettingenHealth2 contains these 420 regions with an individual ID (column district) and geographic coordinates (columns lat and lon, respectively) and the number of general practitioners, psychotherapists and pharmacies located there (columns phys_gen, psych and pharm, respectively) as well as the local population (column pop). First, we load the dataset:

Now, we investigate how the health care providers are dispersed over the whole area. In the first step, we calculate the Gini coefficient for the concentration of general practitioners using the REAT function gini():

[1] 0.8386269

The empirical Gini coefficient is equal to 0.839, indicating a relatively strong concentration. If we want to calculate the normalized (unbiased) indicator instead, we use the same function with the optional argument coefnorm = TRUE:

[1] 0.8406284

In the same way, we calculate e.g. the Herfindahl-Hirschman index, non-normalized and normalized:

[1] 0.01528053

herf (GoettingenHealth2$phys_gen, coefnorm = TRUE)

[1] 0.01293036

Remember that the minimum of HHI is 1∕n (here: 1∕420 ≈ 0.00238) and the minimum of HHI* is equal to zero.

If we want to inspect the concentration graphically, we could use the Lorenz curve, which can be plotted using either the functions gini() or lorenz(). Here, we use gini(), tell the function to plot the curve (lc = TRUE), and include several graphical parameters (such as lc.col for the color of the Lorenz curve or lcx and lcy for the x/y axes labels). As we want to compare the population distribution to the location distribution, we start by plotting the Lorenz curve for the local population:

lc.col = "orange", lcx = "Shares of districts", lcy = "Shares of

providers", lctitle = "Spatial concentration of health care

providers", lcg = TRUE, lcgn = TRUE, lcg.caption =

"Population 2016:", lcg.lab.x = 0, lcg.lab.y = 1)

# Gini coefficient and Lorenz curve for the no. of inhabitants

[1] 0.5840336

Now, we overlay the Lorenz curves of general practitioners and psychotherapists, which means adding two more curves (function argument add.lc = TRUE):

lc.col = "red", lcg = TRUE, lcgn = TRUE, lcg.caption =

"Physicians 2016:", lcg.lab.x = 0, lcg.lab.y = 0.85)

# Adding Gini coefficient and Lorenz curve for the general practitioners

[1] 0.8386269

gini(GoettingenHealth2$psych, lsize = 1, lc = TRUE, add.lc = TRUE,

lc.col = "blue", lcg = TRUE, lcgn = TRUE, lcg.caption =

"Psychotherapists 2016:", lcg.lab.x = 0, lcg.lab.y = 0.7)

# Adding Gini coefficient and Lorenz curve for psychotherapists

[1] 0.9329298

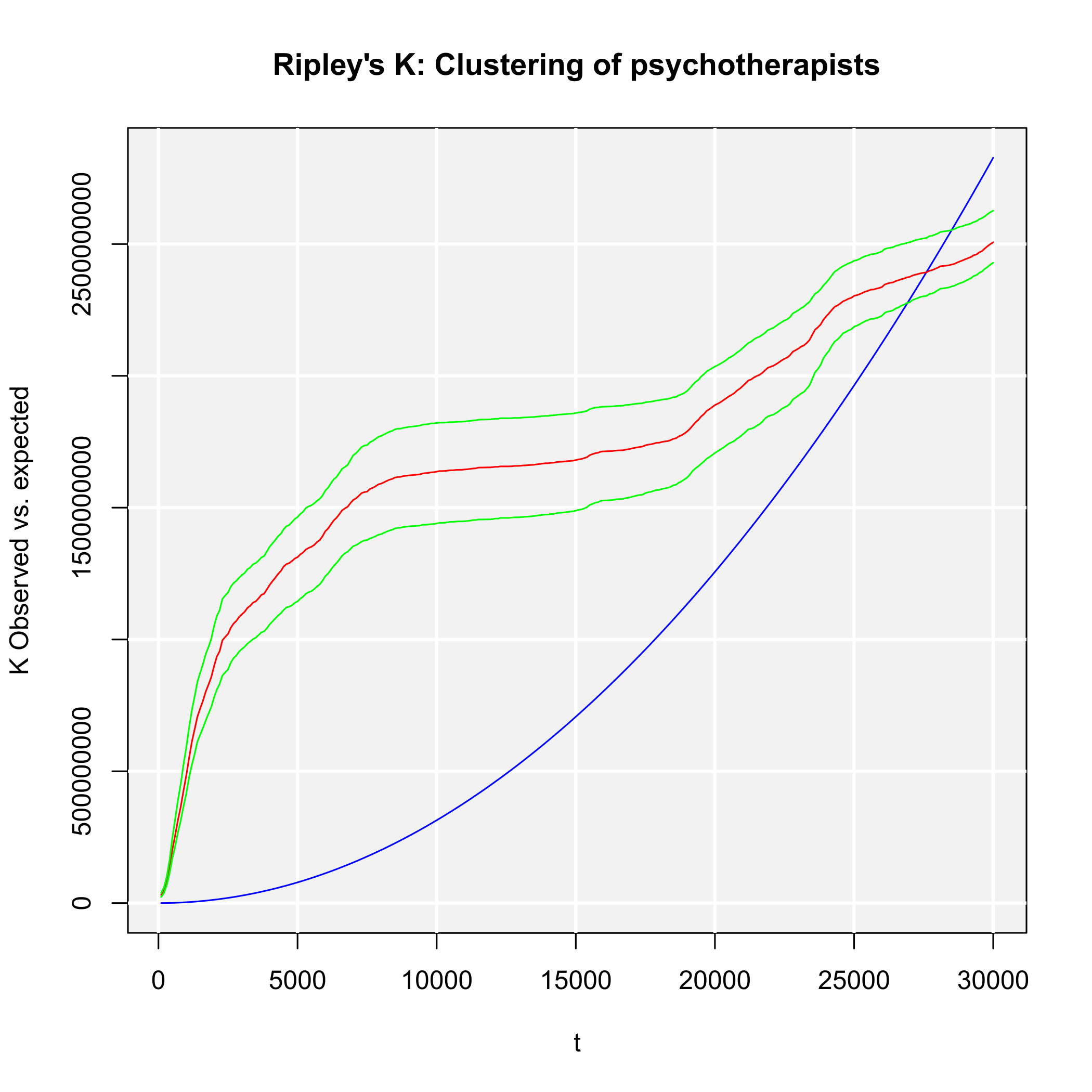

Our commands result in the output of Figure 1, showing three Lorenz curves (population, general practitioners and psychotherapists) and the line of equality (diagonal). All three empirical distributions differ from an equal distribution. In about 72% of the regions, representing about 23% of the whole population (orange curve; G ≈ 0.584), no general practitioner is located (red curve; G ≈ 0.839). But the psychotherapists are more concentrated, as they are located only in about 13% of all districts (blue curve; G ≈ 0.933). As we can see, the physicians are more concentrated than the inhabitants but the psychotherapists are more concentrated than the physicians.

Now, we calculate all mentionened concentration and dispersion coefficients at once for all three types of providers using the function disp(), including a population weighting:

# column 5 = general practitioners, column 6 = psychotherapists,

# column 7 = pharmacies, column "pop" = local population

Our output is:

Note: w = weighted, n = normalized, eq = equivalent number

phys_gen psych pharm

Gini 0.838626907 0.932929782 0.891547619

Gini n 0.840628403 0.935156345 0.893675418

Gini w 0.629454516 0.770895945 0.705628058

Gini w n 0.630956794 0.772735792 0.707312135

HHI 0.015280527 0.038494685 0.024166667

HHI n 0.012930361 0.036199923 0.021837709

HHI eq 65.442769020 25.977611940 41.379310345

Hoover 0.721428571 0.883333333 0.838095238

Hoover w 0.001852337 0.003130602 0.003418787

Theil NA NA NA

Theil w NA NA NA

Coulter 0.049850824 0.123305927 0.065569205

Atkinson 0.761164110 0.900755425 0.854223763

Dalton NA NA NA

SD 1.714506606 1.095496987 0.865286915

SD w 4.010246439 1.847716870 2.401476794

CV 2.330397328 3.899226565 3.028504203

CV n 0.113847359 0.190489683 0.147952112

Williamson 1.429449565 1.965446423 1.709288672

We conclude that any concentration/dispersion measure is the highest for psychotherapists and the lowest for the general practitioners, while the values for pharmacies lie between them. The regional disparities with respect to pharmacies are higher than those with respect to general practitioners, while the most unequal distribution is that of psychotherapists. In other words: The pharmacies are more spatially concentrated than the general practitioners and the psychotherapists are the most concentrated health locations here.

In most cases, population weighting reduces the coefficient values. That is, because districts with a large (small) population have a high (low) impact on the resulting coefficient and the districts without health service providers are also small districts. Furthermore, as the regarded variables contain zero values (which means no health service locations), the Theil coefficient (including the term ln(∕xi)) and the Dalton coefficient (including the n-th root) cannot be computed, resulting in an output of NA.

The visible output of any function presented above can be saved in a new R object:

# save as gini_phys (numeric vector of length = 1)

We can simply access our result:

[1] 0.8386269

The function disp() returns a matrix with 13 rows (when only unweighted coefficients are computed) or 19 rows (in the case of additional weighted coefficients) and one column for each regarded variable:

weighting = GoettingenHealth2$pop)

# save as disp_Goettingen (matrix)

We call our results:

phys_gen psych pharm

Gini 0.83862691 0.93292978 0.89154762

Gini n 0.84062840 0.93515634 0.89367542

...

3 Regional convergence

3.1 The concept of beta and sigma convergence

Regional convergence is derived from (regional) growth theory (for an extensive survey, see Barro, Sala-i Martin 2004) and means the decline of regional disparities over time. The neoclassical growth model states that a region’s economic output (e.g. GDP per capita) depends on its stock of factors of production, capital and labor (aggregate production function), on condition of constant returns to scale and diminishing marginal product of the factor inputs. As a consequence, regions with a high (low) initial level of factor input grow slower (faster) than “poor” (“rich”) regions, what is called beta convergence. It is assumed that all regions converge to the same regional output level (steady-state). Sigma convergence means the decline of regional inequality with respect to regional output over time itself (Allington, McCombie, 2007; Capello, Nijkamp, 2009).

Both types of convergence can be tested empirically, as presented in Table 3. When testing for beta convergence, the natural logarithms of output growth over T time periods in i regions is regressed against the natural logarithms of the initial output values at time t. The original convergence formula was presented by Barro, Sala-i Martin (2004) using a nonlinear least squares (NLS) estimation approach. But in many cases, a linear transformation is used which allows for ordinary least squares (OLS) estimation (Allington, McCombie, 2007; Dapena et al., 2016; Schmidt, 1997; Young et al., 2008). The outcome variable of the convergence equation can be the regional growth between two years (e.g. Young et al. 2008) or the average growth rate per year (e.g. Goecke, Hüther 2016; Puente 2017; Weddige-Haaf, Kool 2017). Significance tests are carried out with t-tests for the regression coefficients and, in the OLS case, the F-test for the significance of R2.

The estimated parameter of interest is the slope of the model, here denoted β (that is why the modeled process is called beta convergence): If β < 0 and statistically significant, there is absolute beta convergence. If additional variables (conditional variables) are included into the convergence equation, we have a test for conditional beta convergence. A further interpretation of the β coefficient is possible using the speed of convergence, λ, and H, the so-called half-life, which means the time (measured in the regarded time periods) to reduce the regional disparities by one half (Allington, McCombie, 2007; Schmidt, 1997).

Sigma convergence (which is named after the Greek letter for the standard deviation, σ) can be tested in two ways depending on the number of time periods: The regional inequality between all regions at time t is measured using the standard deviation, σt, or the coefficient of variation, cvt, for the GDP per capita in its original or natural-logged form. If only two years are regarded, the quotient of both parameters is computed. If e.g. σt1 > σt2, the regional inequality has declined from t1 to t2. A significance test can be applied with a simple ANOVA (analysis of variance), where the test statistic is the quotient of the underlying variances (σ2) (Furceri, 2005; Schmidt, 1997; Young et al., 2008). Within a time series, the dispersion parameter is regressed (and plotted) against time. If the slope coefficient of time is negative, there is sigma convergence (Goecke, Hüther, 2016; Huang, Leung, 2009; Schmidt, 1997).

| Type of convergence | Two time periods | More than two time periods | |

| Beta convergence | absolute

| ||

| and estimation type | NLS | NLS | |

ln( ln( ) = ) = |  ∑

t=1T ln( ∑

t=1T ln( ) = ) = |

||

α - [ ] ln(Y i,t1) + ϵ ] ln(Y i,t1) + ϵ | α - [ ] ln(Y i,t1) + ϵ ] ln(Y i,t1) + ϵ |

||

| OLS | OLS | ||

ln( ln( ) = ) = |  ∑

t=1T ln( ∑

t=1T ln( ) = ) = | ||

| α + β ln(Y i,t1) + ϵ | α + β ln(Y i,t1) + ϵ | ||

| conditional | |||

| NLS | NLS | ||

ln( ln( ) = ) = |  ∑

t=1T ln( ∑

t=1T ln( ) = ) = |

||

α - [ ] ln(Y i,t1) + θXi + ϵ ] ln(Y i,t1) + θXi + ϵ | α - [ ] ln(Y i,t1) + θXi + ϵ ] ln(Y i,t1) + θXi + ϵ |

||

| OLS | OLS | ||

ln( ln( ) = ) = |  ∑

t=1T ln( ∑

t=1T ln( ) = ) = | ||

| α + β ln(Y i,t1) + θXi + ϵ | α + β ln(Y i,t1) + θXi + ϵ | ||

| β < 0 | β < 0 | ||

| Convergence speed: λ =

| |||

| Half-life: H =

| |||

| Sigma convergence | σt =  or or | ||

| cvt =  | |||

> 1 or > 1 or | σ = a + bt + ϵ or | ||

> 1 > 1 | cv = a + bt + ϵ | ||

Test statistic:  | b < 0 | ||

Notes: Y i,t is the regional output (e.g. GDP per capita) of region i at time t, t is the arithmetic mean of Y i,t for all regions at time t, T is the number of regarded time periods (e.g. years), Xi is a set of other variables (conditions), σt is the standard deviation of the regional output of all regions, cvt is the corresponding coefficient of variation, α, β, θ, a and b are estimated coefficients, ϵ is an error term and n is the number of regions.

Compiled from: Allington, McCombie (2007); Barro, Sala-i Martin (2004); Furceri (2005); Schmidt (1997)

3.2 Application in REAT

3.2.1 REAT functions for beta and sigma convergence

Table 4 shows the functions for beta and sigma convergence as implemented in REAT. The analysis of beta convergence is provided by the functions betaconv.ols() and betaconv.nls() for OLS and NLS estimation, respectively. Speed of convergence and half-life can be computed with the function betaconv.speed(). The ratio test of sigma convergence for two time periods can be done using the function sigmaconv(), while a trend regression over time is implemented into the function sigmaconv.t(). Both convergence types can be analyzed at once with the function rca(), which is a wrapper for all functions mentioned above.

The functions require (at least) two numeric vectors, containing the regarded variable Y (e.g. GDP per capita) for at least two different time periods, e.g. from the same data frame. Also the start and end time periods (t1 and tT) have to be stated. Optionally, a graphical output can be generated (scatterplot for beta convergence, line plot for sigma convergence with respect to longitudinal data). Furthermore, when analyzing sigma convergence, the user can choose whether Y should be log-transformed or not and/or which sigma measure is computed (variance, standard deviation or coefficient of variation; weighted or non-weighted).

Note that, unlike the functions for regional inequality indicators (Section 2), the REAT functions for regional convergence distinguish between a visible and an invisible output. The latter can be saved as a new R object. While the visible output shows the main results, the invisible output goes beyond that: betaconv.ols(), betaconv.nls() and rca() return a list, which is the most flexible data type in R, because it consists of a non-predetermined number of different data objects. Apart from the model results, e.g. the (transformed) regression data is returned in this invisible output.

| Convergence | REAT function | Mandatory arguments | Optional arguments | Output |

| Beta | betaconv.ols() | vectors Y i,t1 and | Conditions, | visible: model |

| convergence | Y i,t2,...,Y i,T, | scatterplot | estimates, invisible: | |

| t1 and tT | list with model | |||

| estimates and | ||||

| regression data, | ||||

| optional: plot | ||||

| betaconv.nls() | vectors Y i,t1 and | Conditions, | visible: model | |

| Y i,t2,...,Y i,T, | scatterplot | estimates, invisible: | ||

| t1 and tT | list with model | |||

| estimates and | ||||

| regression data, | ||||

| optional: plot | ||||

| betaconv.speed() | values β | matrix with | ||

| and T | λ and H | |||

| Sigma | sigmaconv() | vectors Y i,t1 and | Sigma measure, | visible: estimates, |

| convergence | (when T = 2) | Y i,t2, t1 and tT | log, weighting, | invisible: matrix |

| normalization | with estimates | |||

| sigmaconv.t() | vectors Y i,t1 and | Sigma measure, | visible: model | |

| (when T > 2) | Y i,t2,...,Y i,T, | log, weighting, | estimates, invisible: | |

| t1 and tT | normalization, | matrix with | ||

| line plot | model estimates, | |||

| optional: plot | ||||

| All at once: | ||||

| Beta and | rca() | vectors Y i,t1 and | Beta estimation, | visible: model |

| sigma | Y i,t2,...,Y i,T, | conditions, | estimates, invisible: | |

| convergence | t1 and tT | scatterplot, | list with model | |

| sigma measure, | estimates and | |||

| log, weighting, | regression data, | |||

| line plot | optional: plot | |||

Source: own compilation.

3.2.2 Application example: Beta and sigma convergence in Germany on the county level

In this example, we look at regional convergence in Germany. The REAT package includes the example dataset G.counties.gdp with the GDP (gross domestic product), the population and the GDP per capita for the 402 counties (“Kreise”) in Germany 1992 to 2014 (complete data only for 2000-2014). First, we load the dataset:

In our case, we prevent scientific notation of numbers in R and set a limit of 4 digits:

We need the columns named gdppcxxxx, containing the GDP per capita for each year, e.g. G.counties.gdp$gdppc2010 contains the GDP per capita for 2010. In the first step, we test absolute beta convergence comparing the years 2010 and 2014 with OLS estimation using the function betaconv.ols():.

2014, output.results = TRUE)

# Two years, no conditions (Absolute beta convergence)

The output is:

Model coefficients (Estimation method: OLS)

Estimate Std. Error t value Pr (>|t|)

Alpha 0.104159 0.018934 5.501 0.00000006743

Beta -0.007373 0.001848 -3.990 0.00007867475

Lambda 0.001850 NA NA NA

Halflife 374.640507 NA NA NA

Model summary

Estimate F value df 1 df 2 Pr (>F)

R-Squared 0.03827 15.92 1 400 0.00007867

We see that both regression coefficients, α and β, are statistically significant (t ≈ 5.50 and -3.99, respectively, both p < 0.001) and the linear regression model is significant as a whole (F ≈ 15.92, p < 0.001). The negative sign of β shows that, on average, the higher the initial GDP per capita, the lower its growth, which indicates absolute beta convergence. However, the convergence process is very slow: The speed of convergence, represented by λ, shows a harmonization by 0.185% per year. This implies that the output gap will be reduced by 50% in approximately 375 years.

Now we check sigma convergence for the same time using the function sigmaconv(). We choose the coefficient of variation as measure, while using the GDP per capita values in their original form:

2014, sigma.measure = "cv", output.results = TRUE)

# Using the coefficient of variation

The output is:

Estimate F value df1 df2 Pr (>F)

CV 2010 0.03416 NA NA NA NA

CV 2014 0.03316 NA NA NA NA

Quotient 1.03004 1.038 401 401 0.7117

The coefficient of variation is a little smaller in 2014, which means the spatial inequality declined between 2010 and 2014. The quotient of the variances is slightly above one (F = σ20102∕σ20142 ≈ 1.04), but not statistically significant (p ≈ 0.71).

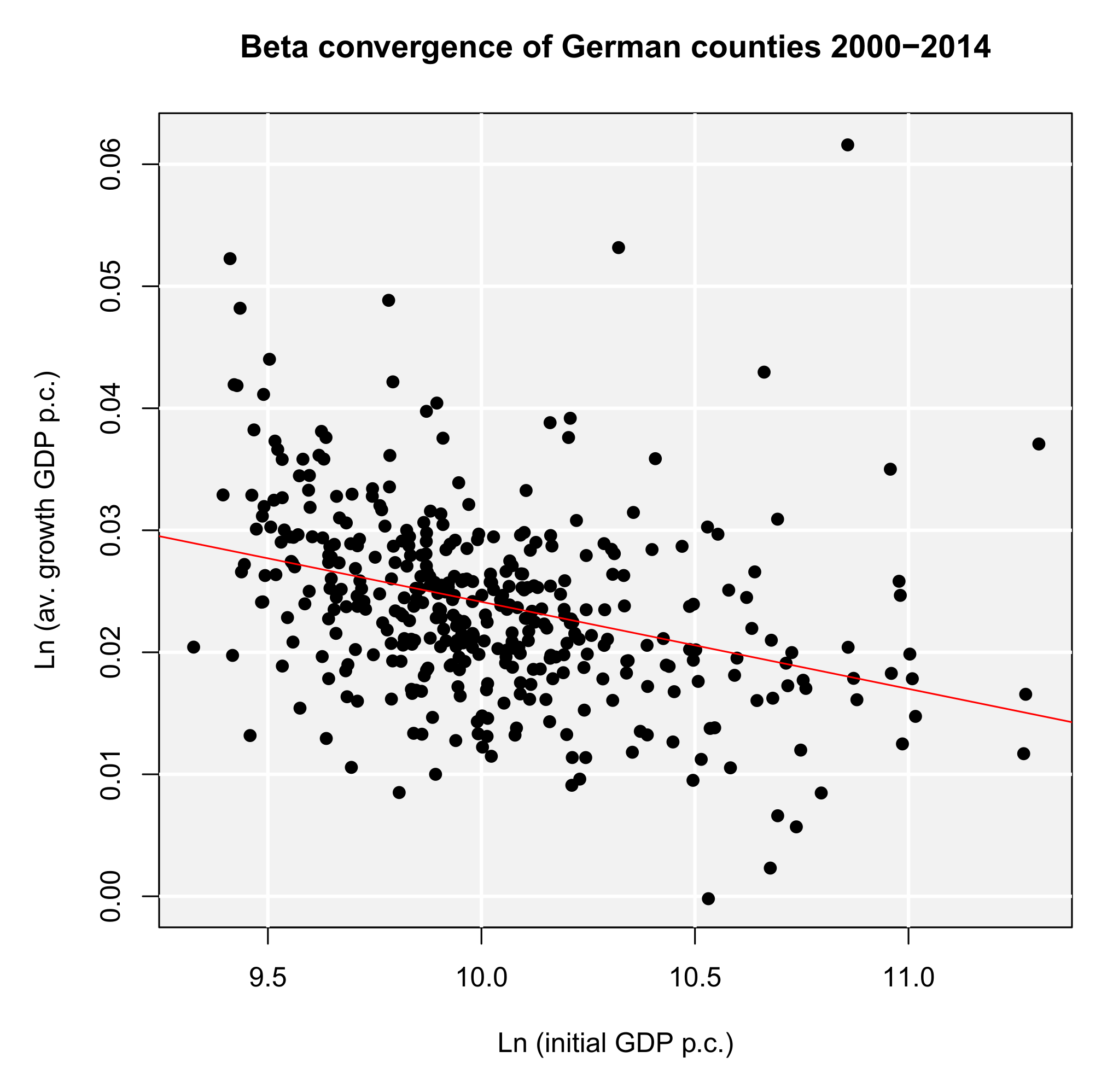

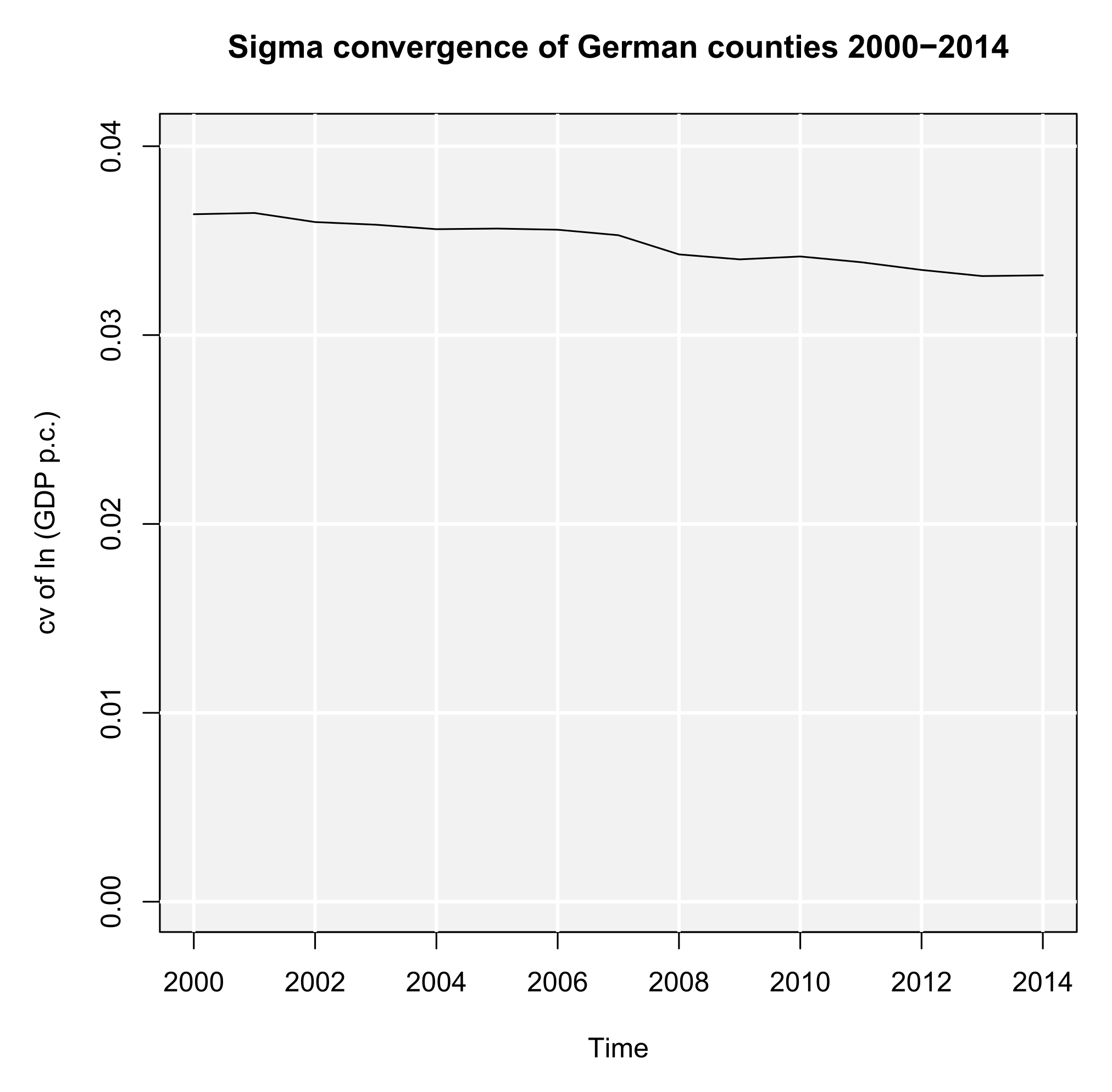

When analyzing regional convergence with REAT, it is preferable (and more convenient) to use the wrapper function rca(). Instead of repeating the results above, we test for (absolute) beta and sigma convergence between 2000 and 2014. The analysis of sigma convergence uses trend regression (function argument sigma.type = "trend") for the coefficient of variation (sigma.measure = "cv"). We also want plots for both convergence types (beta.plot = TRUE and sigma.plot = TRUE, respectively) with specific axis labels (e.g. beta.plotX = "Ln (initial GDP p.c.)"). Our code is:

conditions = NULL, sigma.type = "trend", sigma.measure = "cv",

beta.plot = TRUE, beta.plotLine = TRUE, beta.plotX =

"Ln (initial GDP p.c.)", beta.plotY = "Ln (av. growth GDP p.c.)",

beta.plotTitle = "Beta convergence of German counties 2000-2014",

sigma.plot = TRUE, sigma.plotY = "cv of ln (GDP p.c.)",

sigma.plotTitle = "Sigma convergence of German counties 2000-2014")

# 14 years: 2000 (column 55) to 2014 (column 68)

# no conditions (Absolute beta convergence)

# with plots for both beta and sigma convergence

This results in the following output:

Absolute Beta Convergence

Model coefficients (Estimation method: OLS)

Estimate Std. Error t value Pr (>|t|)

Alpha 0.0954564 0.0099087 9.634 0.00000000000000000006845

Beta -0.0071323 0.0009885 -7.215 0.00000000000271925822550

Lambda 0.0005113 NA NA NA

Halflife 1355.7282963 NA NA NA

Model summary

Estimate F value df 1 df 2 Pr (>F)

R-Squared 0.1152 52.06 1 400 0.000000000002719

Sigma convergence (Trend regression)

Estimate Std. Error t value Pr(>|t|)

Intercept 0.5523659 0.03084855 17.91 0.0000000001526

Time -0.0002579 0.00001537 -16.78 0.0000000003446

Model summary

Estimate F value df 1 df 2 Pr (>F)

R-Squared 0.9558 281.4 1 13 0.0000000003446

This function also produces the plots in Figures 2a and 2b, both showing a declining curve, which is a first indication of both beta and sigma convergence. The beta convergence model is statistically significant (F ≈ 52.06, p < 0.001), as well as the coefficients α (t ≈ 9.63, p < 0.001) and β (t ≈-7.21, p < 0.001). Again, we find evidence for absolute beta convergence because of a negative slope (β ≈-0.007). The trend regression model for sigma convergence is significant (F ≈ 281.4, p < 0.001). The slope is significant and negative (b ≈-0.00026, t ≈ 17.91, p < 0.001), which indicates sigma convergence. However, both types of convergence can be regarded as very slow processes: The half-life value shows that, resulting from the beta convergence model, the regional disparities in GDP per capita will be halved in approximately 1,356 years. When looking at the trend regression, we see that the coefficient of variation declines only by 0.00026 per year. Another aspect is that we only regarded absolute beta convergence, ignoring other spatial effects or the impact of regional policy. The latter is also not considered in neoclassical regional growth theory.

(a) Absolute beta convergence

(a) Absolute beta convergence  (b) Sigma convergence

(b) Sigma convergence

Remembering German reunification, we want to test if there are average growth differences between West Germany and East Germany (former German Democratic Republic), which leads to conditional beta convergence. The dataset G.regions.emp contains the column regional, where the counties are attributed either to West or East Germany, expressed as character string ("West" or "East"). We need to include our condition into the convergence equation. Thus, we use the REAT function to.dummy() to create dummy variables (1/0) out of (nominal scaled) variables, and add the indicator for West Germany (1, otherwise 0) to our data:

# Creating dummy variables for West/East

# regionaldummies[,1] = East (1/0), regionaldummies[,2] = West (1/0)

G.counties.gdp$West <- regionaldummies[,2]

# Adding the dummy variable for West

Now, we test for conditional beta and sigma convergence, including the condition “West”, again using the rca() function, but without plots and using the standard deviation (default setting) instead of the cv for sigma convergence. This time, we save the results in an object:

G.counties.gdp[55:68], 2014, conditions = G.counties.gdp[c(70)],

sigma.type = "trend")

# condition variable "West" in column 70

# Store results in "converg_results"

The output is:

Absolute Beta Convergence

Model coefficients (Estimation method: OLS)

Estimate Std. Error t value Pr (>|t|)

Alpha 0.0954564 0.0099087 9.634 0.00000000000000000006845

Beta -0.0071323 0.0009885 -7.215 0.00000000000271925822550

Lambda 0.0005113 NA NA NA

Halflife 1355.7282963 NA NA NA

Model summary

Estimate F value df 1 df 2 Pr (>F)

R-Squared 0.1152 52.06 1 400 0.000000000002719

Conditional Beta Convergence

Model coefficients (Estimation method: OLS)

Estimate Std. Error t value Pr (>|t|)

Alpha 0.0754412 0.0102354 7.371 0.0000000000009872

Beta -0.0047020 0.0010517 -4.471 0.0000101720129094

West -0.0053559 0.0009745 -5.496 0.0000000693910790

Lambda 0.0003366 NA NA NA

Halflife 2058.9555949 NA NA NA

Model summary

Estimate F value df 1 df 2 Pr (>F)

R-Squared 0.1774 43.04 2 399 0.00000000000000001192

Sigma convergence (Trend regression)

Estimate Std. Error t value Pr(>|t|)

Intercept 3.895236 0.3267817 11.92 0.00000002264

Time -0.001764 0.0001628 -10.84 0.00000007041

Model summary

Estimate F value df 1 df 2 Pr (>F)

R-Squared 0.9003 117.4 1 13 0.00000007041

In the rca() output, we can compare the results of absolute and conditional beta convergence. In the conditional model, the explained variance increases from R2 ≈ 0.12 to R2 ≈ 0.18, which indicates an increased explanatory power of the model due to the added condition variable. Both models are statistically significant, also the β values are negative and significant (p < 0.001 in both cases). The condition “West” is significant (t ≈-5.50, p < 0.001) and negative, which means that, on average, the GDP per capita in West German counties grew slower than in East Germany. These results seem to support the convergence hypothesis from growth theory, but one should not forget that e.g. political aspects (such as the German and/or EU regional policy) are not considered in this simple analysis.

As we have saved the invisible function output, we can access specific parts of our analysis, such as the regression data for the absolute convergence model:

# All results in list converg_results

# converg_results contains list betaconv (beta convergence results)

# betaconv contains data frame regdata (regression data)

ln_initial ln_growth

1 11.002 0.01997436

2 10.552 0.02980133

3 10.283 0.01794207

4 10.090 0.01763444

5 10.287 0.02361006

...

If we want to look at the single sigma values, we can address them via:

# All results in list converg_results

# converg_results contains list sigmaconv (sigma convergence results)

# sigmaconv contains data frame sigma.trend (sigma values)

years sigma.years

gdp1 2000 0.3646

gdppc2001 2001 0.3662

gdppc2002 2002 0.3618

gdppc2003 2003 0.3606

gdppc2004 2004 0.3592

...

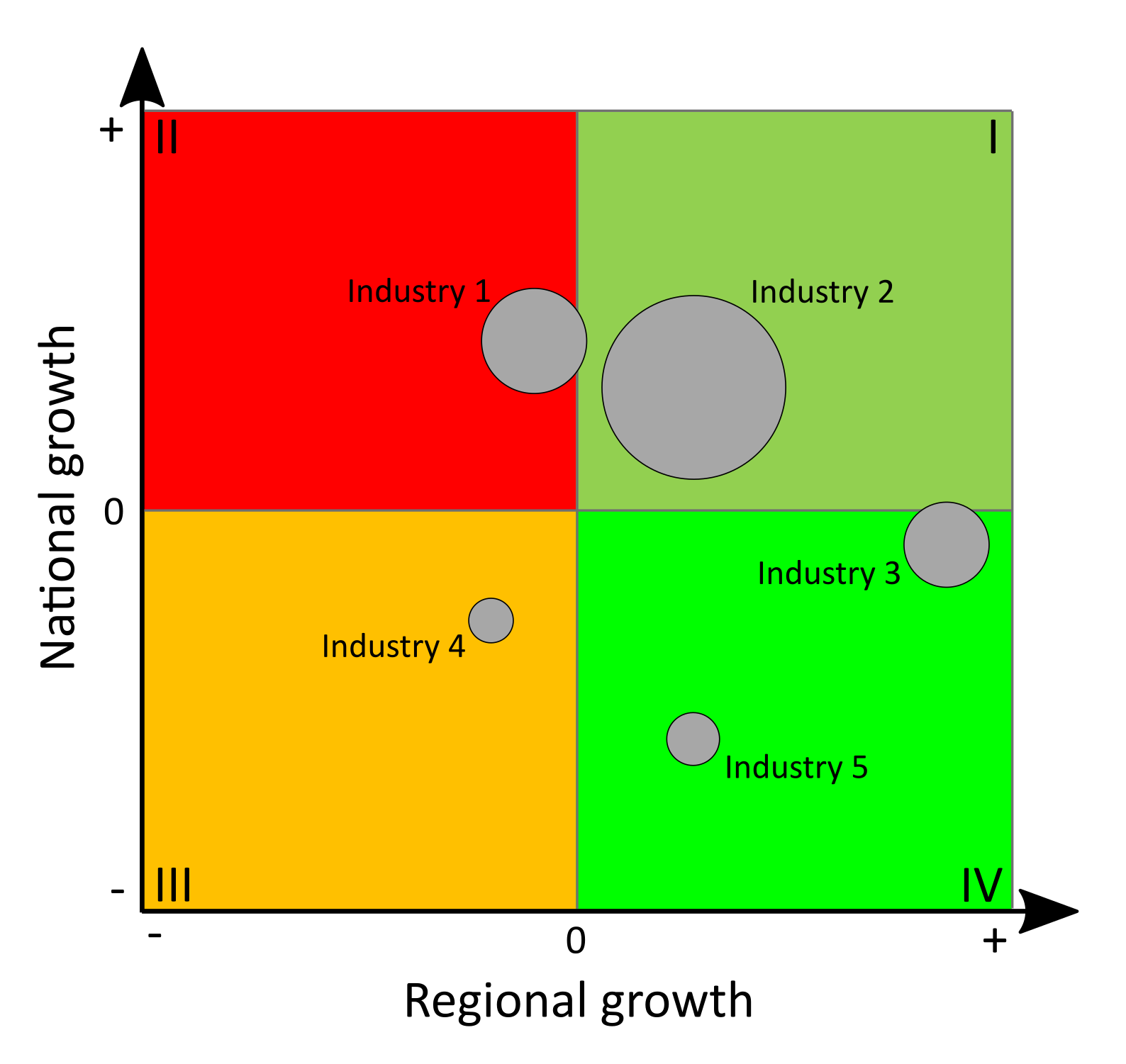

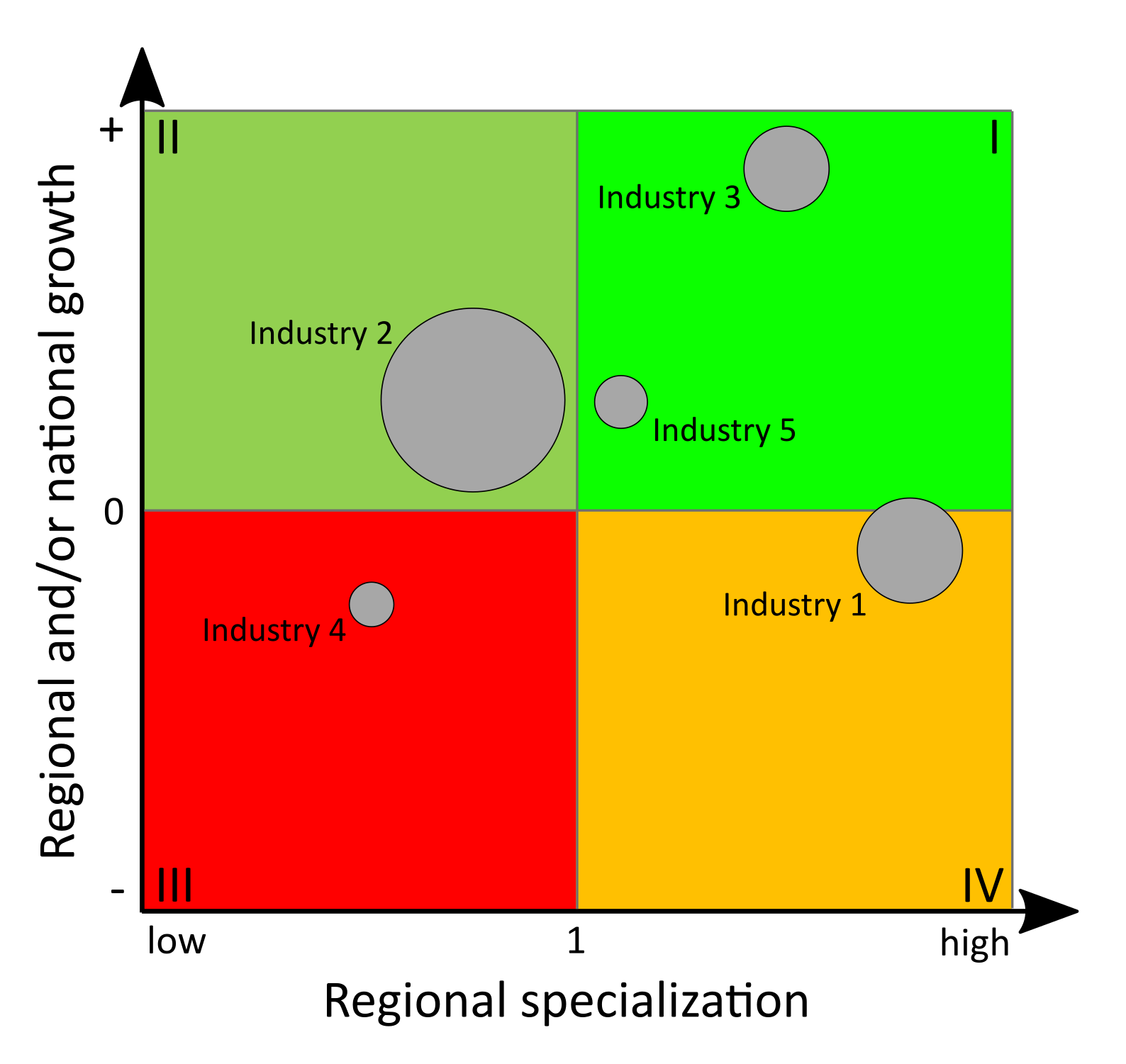

4 Specialization of regions and spatial concentration of industries

4.1 Indicators of regional specialization and industry concentration

Specialization of regions or countries and the spatial concentration of industries or firms are phenomena linked to several research fields in regional economics and economic geography: Specialization is a key point in traditional theories of international trade with respect to comparative advantages (Ricardo, 1821) as well as in the generation of the “New Trade Theory” (introduced by Krugman 1979). Spatial clustering of firms or industries due to agglomeration economies is a perennial issue in all spatial economic fields. It especially reemerged in the context of the “New Economic Geography” (e.g. Krugman 1991; Fujita et al. 2001) as well as through the work of Porter (1990) regarding clusters. The common indicators are broadly discussed in Farhauer, Kröll (2014) or Nakamura, Morrison Paul (2009). For studies comparing some different indicators, see e.g. Goschin et al. (2009); Moga, Constantin (2011); Palan (2017).

When looking at the family of indicators of regional specialization and industry concentration, we have to distinguish between indicators for aggregate data, such as regional employment data, and those requiring individual firm data. The first group, compiled in Table 5, can be differentiated into indicators of specialization and indicators of spatial concentration. As both types of agglomeration are closely linked to each other, so are the corresponding indicators. The empirical basis of all those measures is the employment e in industry i in region j, eij. This employment stock is compared to some reference, mostly including the total employment in region j, ej, and/or the total employment in industry i, ei, as well as the all-over employment e. The individual firm level indicators in Table 6 can be segmented into indicators for agglomeration of one industry due to localization economies and indicators for the coagglomeration of different industries due to urbanization economies.

| Indicator | Specialization of region j | Spatial concentration of industry i |

| Hoover/Balassa | LQij =  ≡ MRCAij = ≡ MRCAij =  |

|

LQj =  ∑

i=1ILQij ∑

i=1ILQij | LQi =  ∑

j=1JLQij ∑

j=1JLQij |

|

| Extensions: | ||

| O’Donoghue-Gleave | SLQij =  |

|

| Tian | SLLQij =  |

|

| Hoen-Oosterhaven | ARCAij =  - - |

|

| Hoover | Hj =  [∑

i=1I| [∑

i=1I| - - |] |] | Hi =  [∑

j=1J| [∑

j=1J| - - |] |] |

| 0 ≤ Hj ≤ 1 | 0 ≤ Hi ≤ 1 | |

| Gini | Gj =  ∑

i=1Iλi(Ri -) ∑

i=1Iλi(Ri -) | Gi =  ∑

j=1Jλj(Cj -) ∑

j=1Jλj(Cj -) |

| 0 ≤ Gj ≤ 1 | 0 ≤ Gi ≤ 1 | |

where: Ri =  , , | where: Cj =  , , |

|

=  ∑

i=1IRi and ∑

i=1IRi and | =  ∑

j=1JCj and ∑

j=1JCj and |

|

| λi = 1,...,I (λi < λi+1) | λj = 1,...,J (λj < λj+1) | |

| Krugman | Kjl = ∑ i=1I|sijs - sils| | Kiu = ∑j=1J|sijc - sujc| |

| (J = 2, I = 2) | 0 ≤ Kjl ≤ 2 | 0 ≤ Kiu ≤ 2 |

where: sijs =  and sils = and sils =  | where: sijc =  and sujc = and sujc =  |

|

| Extensions: | ||

| Midelfart et al., | Kj = ∑ i=1I|sijs -ils| | Ki = ∑j=1J|sijc -ujc| |

| Vogiatzoglou | 0 ≤ Kj ≤ 2 | 0 ≤ Ki ≤ 2 |

| (J > 2, I > 2) | where: sijs =  and and | where: sijc =  and and |

ils =  ∑

iJsils, ∑

iJsils, | ujc =  ∑

uIsujc, ∑

uIsujc, |

|

| l≠j | u≠i | |

| Duranton-Puga | RDIj =  | |

where: sijs =  and si = and si =  | ||

| Litzenberger-Sternberg | CIij =  |

|

where ISij =  , IDij = , IDij =  |

||

and PSij =  |

||

Notes: eij and eil equal the employment of industry i in regions j and l, respectively, ei is the total employment in industry i, euj ist the employment of industry u in region j, ej is the total employment in region j, e is the total employment in the whole economy, I is the number of industries, J is the number of regions, aj is the area of region j, a is the total area in the whole economy, pj is the population in region j, p is the total population, bij is the number of firms of industry i in region j and bi is the number of firms in industry i.

Compiled from: Farhauer, Kröll (2014); Hoen, Oosterhaven (2006); Hoffmann et al. (2017); Nakamura, Morrison Paul (2009); O’Donoghue, Gleave (2004); Tian (2013); Schätzl (2000); Störmann (2009)

| Indicator | Agglomeration | Coagglomeration |

| Ellison-Glaeser | γi =  | γc =  |

| where: Gi = ∑ j=1J(sijc - sj)2, | where: G = ∑j=1J(xj - sj)2, | |

sijc =  , sj = , sj =  and and | xj = ∑

i=1U , sj = , sj =  , si = , si =  |

|

HHIi = ∑

k=1K( )2 )2 | and HHIU = ∑ i=1Usi2HHIi | |

| z-standardization: | ||

zi =  |

||

where: var(Gi) = 2 HHIi2 HHIi2 ∑

j=1Jsj2 ∑

j=1Jsj2 |

||

-2 ∑

j=1Jsj3 + (∑j=1Jsj2)2![]](267115x.png) - - |

||

∑

k=1Kzik4 ∑

j=1Jsj2 - 4 ∑j=1Jsj3 ∑

j=1Jsj2 - 4 ∑j=1Jsj3 |

||

+3(∑

j=1Jsj2)2![]](267117x.png)  |

||

| Howard et al. | CLab =  |

|

| XCLab = CLab - CLabRND | ||

| where: Ckl = 1 if firms k and l are located | ||

| in the same region and Ckl = 0 otherwise | ||

Notes: eij is the employment of industry i in region j, ei is the total employment in industry i, ej is the total employment in region j, e is the total employment in the whole economy, eik is the employment of firm k from industry i, k and l are indices for single firms, I is the number of industries, J is the number of regions, U is a subset of all I industries (U ≤ I), K is the number of firms and Ka and Kb are the numbers of firms in industry a and b.

Compiled from: Farhauer, Kröll (2014); Howard et al. (2016); Nakamura, Morrison Paul (2009)

The most popular indicator is the Location Quotient (LQ), which is attributed to Hoover (1936) and mathematically equivalent to the Revealed Comparative Advantage (RCA) index, developed by Balassa (1965) in the context of international trade. The LQ is utilized in many studies (e.g. Bai et al. 2008; Kim 1995) as well as in the OECD Territorial Reviews (OECD, 2019). Following O’Donoghue, Gleave (2004) and Tian (2013), the original formulation can be extended: As the location quotient is not normalized, there is no cut-off value for defining a cluster, which leads to a standardization of the computed values via z-transformation. Hoen, Oosterhaven (2006) developed an additive alternative to the RCA index. The original LQ provides the main mathematical basis for several indicators developed later, such as the spatial Gini coefficients described below.

Some indicators which are known from the context of regional inequality (see Section 2) are also used for the analysis of agglomeration: A modification of the Gini coefficient is used for the spatial concentration of industries as well as regional specialization (e.g. Ceapraz 2008; Wieland, Fuchs 2018). As we can see in the calculation of Ri and Cj, respectively, the spatial Gini coefficient is based on the LQ. Another popular option for analyzing agglomeration is the Hoover coefficient, comparing the structure of an industry/a region to a reference structure of all industries/regions (e.g. Dixon, Freebairn 2009; Jiang et al. 2007). Both indicator types range between zero (no specialization/concentration) and one (total specialization/concentration). Also the Herfindahl-Hirschman index and its derivates are used to measure concentration, specialization and diversification (e.g. Duranton, Puga 2000; Goschin et al. 2009; Lehocký, Rusnák 2016).

Another type of specialization/concentration indicator was introduced by Krugman (1991), originally designed for comparing the specialization of two regions. An extension of this indicator was established by Midelfart-Knarvik et al. (2000) for the comparison of regional specialization/industry concentration with respect to the sum or mean of all regions/industries (furthermore used e.g. by Haas, Südekum 2005; Vogiatzoglou 2006). Unlike the Gini- or Hoover-type measures, the Krugman coefficients range between zero (no specialization/concentration) and two (total specialization/concentration).

The cluster index developed by Litzenberger, Sternberg (2006) goes beyond employment data and includes additional information about the industry-specific firm size, population density and region size. It is composed of three parts: the relative industrial stock with respect to industry i and region j, ISij, the relative industrial density, IDij, and the relative firm size, PSij. All three components are modified location quotients. This is done to control for small and monostructural regions, which are identified as clusters otherwise (which is a problem in the original LQ). The cluster index CIij has a potential range from zero to infinity. This extended indicator is used e.g. by Hoffmann et al. (2017) for the German food processing industry.

The cluster indicators by Ellison, Glaeser (1997) compare the empirical distribution of firms to an arbitrary location pattern where agglomeration economies are absent (often referred to as a dartboard approach). Ellison, Glaeser (1997) differentiate between the clustering of firms from one industry (agglomeration) due to localization economies and the clustering of multiple industries (coagglomeration) due to urbanization economies. Their indices also take into account the industry-specific structure of the firms by including the Herfindahl-Hirschman index, HHIi, for the employment concentration in industry i. This is the reason why individual firm-level data is required for the computation. The Herfindahl-Hirschman indicator is included to control the raw measures of spatial concentration, Gi and G, for firm employment concentration, which occurs especially when there are just a few firms with many employees. The Ellison-Glaeser (EG) index for agglomeration, γi, is designed for identifying the clustering of industry i, while the coagglomeration index, γc aims at the clustering of a set of U industries, where U ≤ I. Values of γ equal to zero imply the absence of agglomeration economies, while values above zero indicate positive effects due to spatial clustering. When γ is negative, firm locations are less spatially concentrated than expected on condition of the dartboard approach, which indicates negative agglomeration economies. The EG index is used in several current regional economic studies (e.g. Dauth et al. 2015, 2018; Yamamura, Goto 2018).

In contrast, Howard et al. (2016) argue that agglomeration economies should not be analyzed regarding employment but the firms itself. Their colocation index, CLab, sums the colocation of Ki and Kq firms from two industries, i and q, controlling for all possible combinations. This colocation measure is compared to a counterfactual location structure constructed via bootstrapping; specifically the arithmetic mean of a number of (e.g. 50) random assignments of the regarded firms to the locations. The value of the resulting excess colocation index, XCLab, ranges between -1 and 1.

4.2 Application in REAT

4.2.1 REAT functions for regional specialization and industry concentration

Table 7 shows the REAT functions for agglomeration measures based on aggregate (employment) data. All functions require at least information about the employment in one or more regions j in one or more industries i, eij. The Herfindahl-Hirschman index (function herf()) for measuring regional diversity is not displayed as it is used exactly in the same way as described in Section 2, replacing xi with eij.

| Indicator | REAT function | Mandatory arguments | Optional arguments | Output |

| Hoover LQ/ | locq() | vectors or single | LQ method, | Single value or |

| Balassa RCA | values of eij and ei, | plot | matrix with LQij | |

| incl. extensions | single values of | |||

| ej and e | ||||

| locq2() | vectors of eij, | normalization, | matrix or data | |

| industry ID i | output type, | frame with I * J | ||

| and region ID j | remove NAs | values of LQij | ||

| Hoover | hoover() | vectors of eij | remove NAs | value: Hj |

| specialization/ | (see Section 2) | and reference | or Hi | |

| concentration | vector ei or ej | |||

| Gini | gini.spec() | vectors eij | plot LC | value: Gj, |

| specialization | and ei | optional: LC plot | ||

| concentration | gini.conc() | vectors eij | plot LC | value: Gi, |

| and ej | optional: LC plot | |||

| Krugman | krugman.spec() | vectors eij | value: Kjl | |

| specialization | (regions j and l) | and eil | ||

| krugman.conc2() | vector eij and matrix | value: Kj | ||

| (all J regions) | or data frame eil | |||

| concentration | krugman.conc() | vectors eij | value: Kiu | |

| (industries i and u) | and euj | |||

| krugman.conc2() | vector eij and matrix | value: Ki | ||

| (all I industries) | or data frame euj | |||

| All at once: | ||||

| specialization | spec() | vectors of eij, | remove NAs | matrix with Hj, Gj |

| industry ID i | and Kj (columns) | |||

| and region ID j | for J regions (rows) | |||

| concentration | conc() | vectors of eij, | remove NAs | matrix with Hi, Gi |

| industry ID i | and Ki (columns) | |||

| and region ID j | for I industries (rows) | |||

| Duranton- | durpug() | vectors eij | value: RDIj | |

| Puga | and ei | |||

| Litzenberger- | litzenberger() | single values of | value: CIij | |

| Sternberg | eij, ei, aj, a, | |||

| pj, p, bij and bi | ||||

| litzenberger2() | vectors of eij, | output type, | matrix or data | |

| industry ID i, | remove NAs | frame with I * J | ||

| region ID j, | values of CIij | |||

| aj, pj and bij | ||||

Source: own compilation.

Location quotients for one region and one or more industries are computed by the function locq(), including the option for an additive indicator instead of the multiplicative. When calculating the LQ for a set of J regions and I industries, one can use function locq2(), which is a kind of batch processing extension of locq(). As the dimension of the Litzenberger-Sternberg cluster index is the same as in the LQ (a single value for each combination of region j and industry i), the related functions litzenberger() and litzenberger2() work in the same way. When using locq2() or litzenberger2(), the user may choose the type of function output: either a matrix with I columns and J rows or a data frame with I * J rows.

The Hoover-, Gini- and Krugman-type indicators require the same kind of input data. The hoover() function was already explained in Section 2, as it can be also used for measuring spatial concentration of industries or the specialization of regions with all-over employment vectors, ei and ej, respectively, as reference distributions. The spatial Gini coefficients are available through functions gini.spec() for regional specialization and gini.conc() for spatial concentration. The Krugman coefficients are divided into functions for the comparison of two regions/industries (krugman.spec() and krugman.conc(), respectively) and for applying all regions/industries as reference (krugman.spec2() and krugman.conc2(), respectively). The functions spec() and conc() are wrapper functions providing a convenient way to compute Hoover, Gini and Krugman coefficients of a given set of J regions and I industries at once, e.g. originating from official statistics on regional employment.

| Indicator | REAT function | Mandatory arguments | Optional arguments | Output |

| Ellison-Glaeser | ellison.a() | vectors of eik, ej | visible: value γi, | |

| agglomeration | and region ID j | invisible: matrix with γi, | ||

| Gi, zi, Ki and HHIi | ||||

| ellison.a2() | vectors eik, | visible: values γi, | ||

| industry ID i and | invisible: matrix with γi, | |||

| region ID j | Gi, zi, Ki and HHIi, | |||

| for I industries (rows) | ||||

| coagglomeration | ellison.c() | vectors eik, | vectors ej and | value: γc |

| industry ID i and | U industries | |||

| region ID j | ||||

| ellison.c2() | vectors eik, | vector ej | matrix with γc for | |

| industry ID i and | I * I - I industry | |||

| region ID j | combinations (rows) | |||

| Howard et al. | howard.cl() | firm ID k, | value: CLab | |

| colocation | industry ID i, | |||

| and region ID j, | ||||

| industries a and b | ||||

| excess | howard.xcl() | firm ID k, | value: XCLab | |

| colocation | industry ID i | |||

| and region ID j, | ||||

| industries a and b, | ||||

| no. of samples | ||||

| howard.xcl2() | firm ID k, | matrix with XCLab for | ||

| industry ID i | I * I - I industry | |||

| and region ID j | combinations (rows) | |||

Source: own compilation.

Table 8 shows the functions operating on the level of individual firm data. The Ellison-Glaeser (EG) indices are available through the functions ellison.a() (agglomeration index for industry i) and ellison.a2() (agglomeration indices for I industries) as well as ellison.c() (coagglomeration index for U industries) and ellison.c2() (coagglomeration indices for I * I - I industry combinations). All functions require the firm size (e.g. no. of employees) for the k-th firm from industry i (numeric vector) and the region j the firm is located in. The functions incorporating more than one industry (all except for ellison.a()) require a vector containing the industry i. The data could e.g. be stored in a data frame with at least three columns (firm size, region, industry). Like some of the convergence functions (see Section 3), the EG agglomeration index functions in REAT also distinguish between a visible and an invisible output: ellison.a() and ellison.a2() show the value(s) auf γi but return an invisible matrix including the raw measure of concentration (Gi), the z-standardized results (zi) and the related Herfindahl-Hirschman index for industry-specific firm concentration (HHIi) as well as the number of firms in industry i (Ki).

The Howard-Newman-Tarp coagglomeration measure is distributed over the functions howard.cl() (calculation of the colocation index for one pair of industries a and b), howard.xcl() (calculation of the excess colocation index for industries a and b) and howard.xcl2() (calculation of the excess colocation index for I * I - I combinations of I industries). As this cluster index works with firms instead of employment, we only need a vector containing the IDs of the firms k, the corresponding industry i and the region j where the firm is located. When calculating this measure for one pair of industries, the user must state the IDs of industries a and b. Note that calculation time for this index increases heavily with the number of firms and/or industries.

4.2.2 Application example 1: Regional specialization of Göttingen

We use the German classification of economic activities (WZ2008) on the level of 21 sections (A-U) for the classification of industries in the following examples (see Table 9).

WZ2008 | |

| Code | Title |

| A | Agriculture, forestry and fishing |

| B | Mining and quarrying |

| C | Manufacturing |

| D | Electricity, gas, steam and air conditioning supply |

| E | Water supply; sewerage, waste management and remediation activities |

| F | Construction |

| G | Wholesale and retail trade; repair of motor vehicles and motorcycles |

| H | Transportation and storage |

| I | Accommodation and food service activities |

| J | Information and communication |

| K | Financial and insurance activities |

| L | Real estate activities |

| M | Professional, scientific and technical activities |

| N | Administrative and support service activities |

| O | Public administration and defence; compulsory social security |

| P | Education |

| Q | Human health and social work activities |

| R | Arts, entertainment and recreation |

| S | Other service activities |

| T | Activities of households as employers; undifferentiated goods-and services-producing |

| activities of households for own use | |

| U | Activities of extraterritorial organisations and bodies |

Source: own compilation based on Statistisches Bundesamt (2008).

Starting with a simple example, we analyze the regional specialization of Göttingen, a city with a population of about 134,000 in Niedersachsen, Germany. The example dataset Goettingen, which is included in REAT, contains the dependent employees in Göttingen and Germany for 2008 to 2017 in industries A to R (rows 2 to 16; row 1 contains the all-over employment). First, we load the data:

Using the REAT function locq(), we calculate a location quotient for Göttingen with respect to the manufacturing industry (”Verarbeitendes Gewerbe”), which is represented by letter C:

Goettingen$BRD2017[4], Goettingen$BRD2017[1])

# Industry: manufacturing (letter C) in row 4

# row 1 = all-over employment

[1] 0.5369

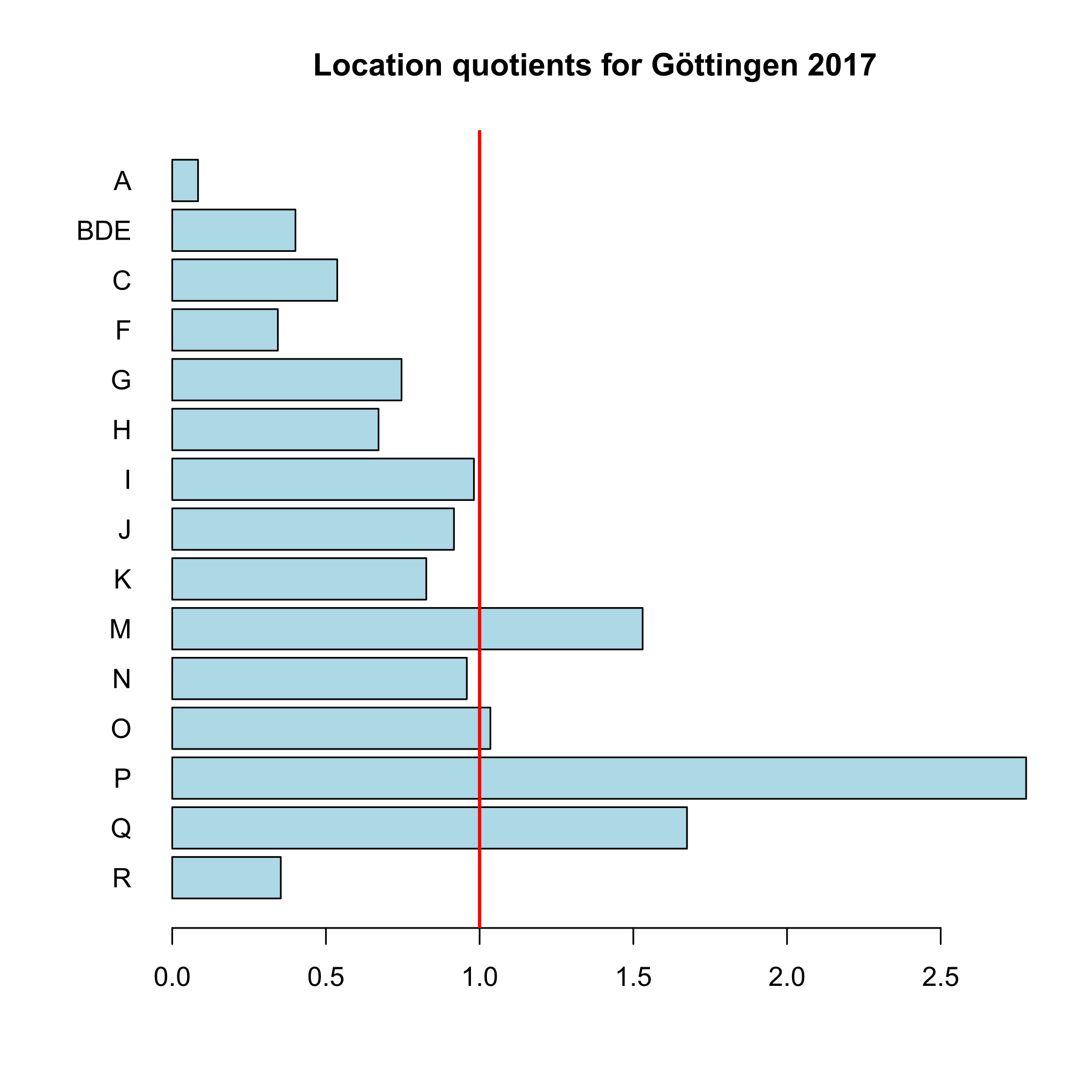

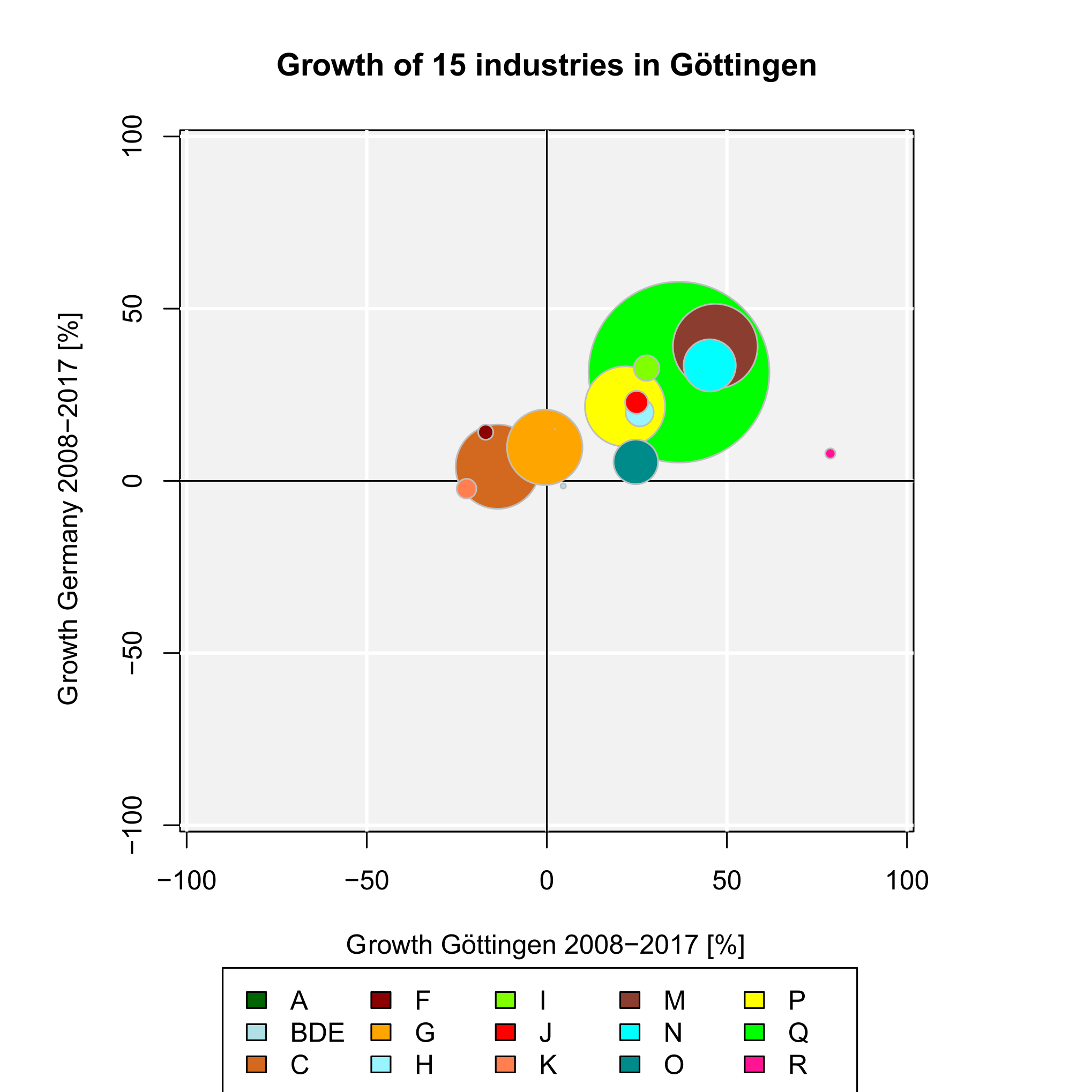

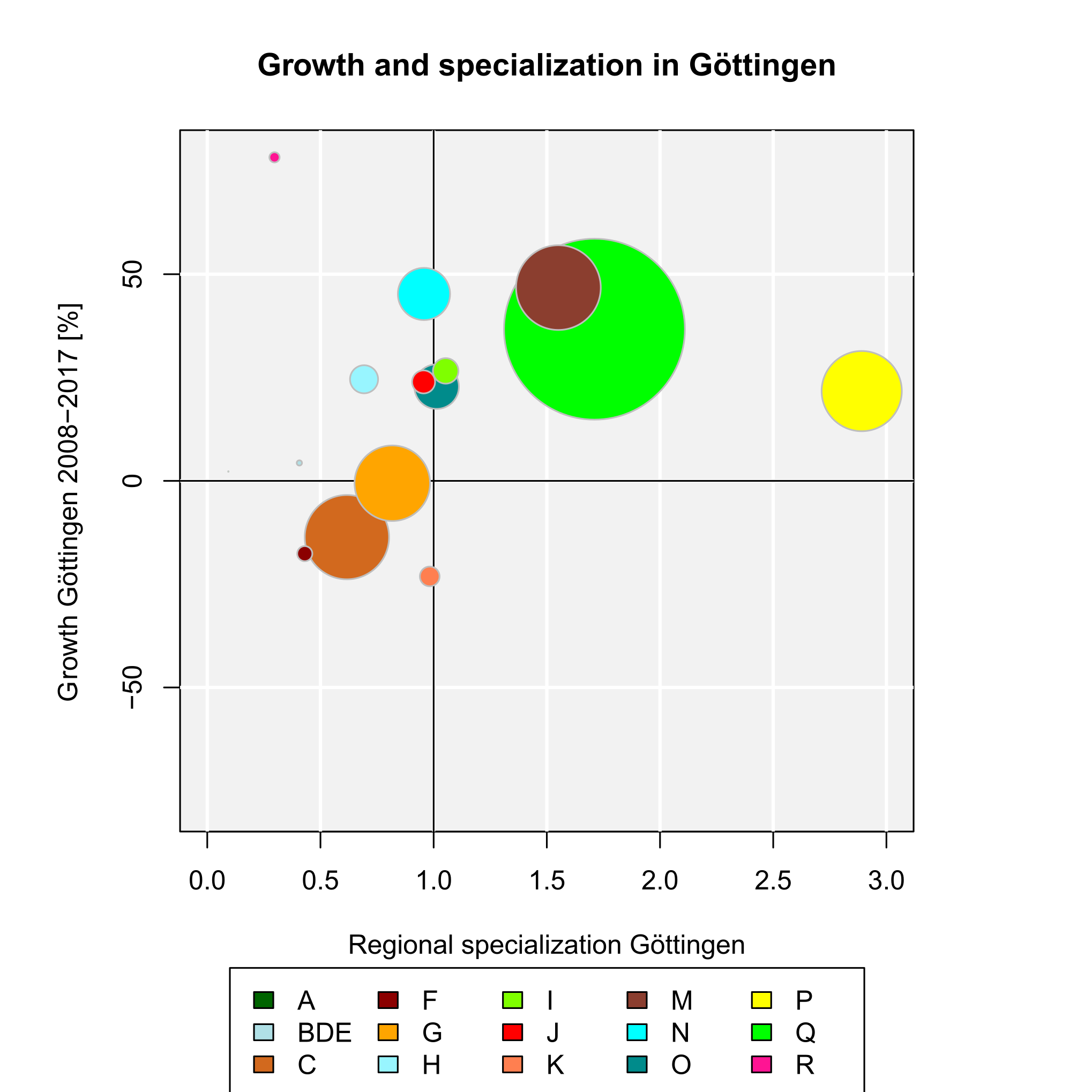

The output is simply the LQ value (LQij, where i is manufacturing and j is Göttingen). We see that the LQ is very low, indicating that manufacturing is underrepresented in Göttingen as compared to Germany. Now, we calculate LQ values for all industries (A-R), including a simple plot (function argument plot.results = TRUE):

Goettingen$BRD2017[2:16], Goettingen$BRD2017[1],

industry.names = Goettingen$WZ2008_Code[2:16], plot.results = TRUE,

plot.title = "Location quotients for Göttingen 2017")

# all industries (rows 2-16 in the dataset)

The output is a matrix with one row for each industry:

I = 15 industries

LQ

A 0.08407652

BDE 0.40085663

C 0.53687366

F 0.34366928

G 0.74603541

H 0.67117311

I 0.98141916

J 0.91654277

K 0.82650178

M 1.53027645

N 0.95843423

O 1.03509027

P 2.77790858

Q 1.67459967

R 0.35317012

The result is plotted in Figure 3. The function plots a vertical line at LQij = 1 automatically. This is the (only) reference value for the LQ. It indicates a stock of the related industry equal to the whole economy. The highest LQ values can be found for the industries with letters P (education) and Q (health). This is because Göttingen is mainly characterized by a large university (about 30,000 students) with a university hospital with about 7,000 employees.

Now, we want to measure the specialization of Göttingen with a single indicator. First, we simply use the Herfindahl-Hirschman coefficient for both Göttingen and Germany using the function herf():

[1] 0.127314

herf(Goettingen$BRD2017[2:16])

[1] 0.1104567

The HHI for Göttingen is slightly larger than for Germany, which indicates a higher specialization (or lower economic diversity) of the region. To combine this information in one indicator, we calculate the Hoover coefficient of specialization using the function hoover(), where the reference distribution is the German industry structure:

[1] 0.2254234

We finish our analysis of Göttingen’s regional specialization by calculating both the Gini and the Krugman coefficient of regional specialization with the same data, using the REAT functions gini.spec() and krugman.spec(), respectively. Note that, here, we use the Krugman coefficient to compare the industry structure of Göttingen to the structure of whole Germany (instead of another region within the country, for which this coefficient was originally formulated):

[1] 0.359852

krugman.spec(Goettingen$Goettingen2017[2:16], Goettingen$BRD2017[2:16])

[1] 0.4508469

There seems to be some specialization in Göttingen, but, unfortunately, we do not have any real reference value to interpret the results.

4.2.3 Application example 2: Identifying clusters in Germany using aggregate data

In this example, we will compute indicators of regional specialization and industry concentration for a set of J regions and I industries at once. We load the included test dataset G.regions.industries containing employment and firms on the level of I = 17 industries (WZ2008 codes B-S) and J = 16 regions (“Bundesländer”) in Germany:

The number of employees in the column emp_all includes dependent employees and self-employed persons. The classification code of industries (see Table 9) can be found in column ind_code, while the region code (abbreviation of the region’s official name) is in column region_code. First, we want to detect the spatial concentration of the 17 industries in Germany by calculating Hoover, Gini and Krugman coefficients for all industries at once, applying the REAT function conc() which is a wrapper function for the mentioned indicators. We save our output in the matrix object conc_i:

industry.id = G.regions.industries$ind_code,

region.id = G.regions.industries$region_code)

The output is:

I = 17 industries, J = 16 regions

H i G i K i

WZ08-B 0.22959050 0.42334831 0.45675385

WZ08-C 0.09933363 0.17047620 0.26813759

WZ08-D 0.07754576 0.12509360 0.16260016

WZ08-E 0.11972072 0.16742909 0.20369011

WZ08-F 0.07676634 0.15357575 0.16996098

WZ08-G 0.03034962 0.05471323 0.07977056

WZ08-H 0.06006957 0.11921850 0.10076748

WZ08-I 0.05177262 0.09939075 0.11450791

WZ08-J 0.10230712 0.22605802 0.24450967

WZ08-K 0.08982871 0.17610712 0.20565974

WZ08-L 0.09798632 0.16784764 0.17472656

WZ08-M 0.06490185 0.14760918 0.14931991

WZ08-N 0.06714816 0.08575299 0.09053327

WZ08-P 0.03019678 0.05053848 0.07043586

WZ08-Q 0.04679962 0.06170335 0.06406058

WZ08-R 0.09424708 0.16748405 0.17023603

WZ08-S 0.04507988 0.07246697 0.06441360

The function returns a matrix with 17 rows (one for each industry) and three columns: H i is the Hoover coefficient, G i is the Gini coefficient and K i is the Krugman coefficient for industry i. We cannot interpret or compare all of these results, but we may pick out some findings: The strongest spatial concentration is found with respect to mining and quarrying (WZ08-B), no matter which indicator is regarded, which may be interpreted with “natural advantages” due to the spatial distribution of mineral resources in Germany. Services (such as retailing) as well as education and health are least concentrated, as these industries are bound to regional demand and/or their locations are regulated by policy and planning authorities.

At a first glance, the three indicators seem to produce similar results. Now, we want to test the similarity between Hoover, Gini and Krugman coefficients of concentration. As we saved our result matrix, we now calculate Pearson correlation coefficients (r) for each pair of indicators using the basic R function cor(), which is implemented in the stats package (included automatically in any R release). The function is applied to the three columns of conc_i, producing a 3 * 3 correlation matrix:

H i G i K i

H i 1.0000000 0.9676518 0.9527747

G i 0.9676518 1.0000000 0.9681770

K i 0.9527747 0.9681770 1.0000000

As we can see, each combination of the three indicators shows a strong positive correlation (Hi vs. Gi: r ≈ 0.97, Hi vs. Ki: r ≈ 0.95, Gi vs. Ki: r ≈ 0.97). At least in this context, we may conclude that these indicators are interchangeable. However, we have to recognize that the analysis presented here is on a large-scale regional level (German “Bundesländer”) and all of the mentioned indicators are affected by the modifiable areal unit problem, which means that the results depend on the aggregation unit in the analysis (see e.g. Dapena et al. 2016 for a discussion of this effect).

Now, we do exactly the same with respect to regional specialization of the 16 regions, using the same data. Analogously, we use the wrapper function spec() for calculating Hoover, Gini and Krugman coefficients of regional specialization, also saving the resulting matrix:

industry.id = G.regions.industries$ind_code,

region.id = G.regions.industries$region_code)

The output is:

I = 17 industries, J = 16 regions

H j G j K j

BB 0.11530353 0.20632682 0.18555259

BE 0.17891265 0.29040841 0.34552331

BW 0.08024011 0.10300695 0.22675612

BY 0.05008135 0.07659148 0.16019603

HB 0.09502615 0.18563500 0.17467291

HE 0.05494422 0.12160142 0.11282696

HH 0.16413456 0.22616814 0.33190321

MV 0.13270849 0.18974606 0.22056868

NI 0.03772799 0.08237225 0.07972852

NW 0.02940091 0.05997505 0.07181569

RP 0.04793147 0.07432361 0.12036513

SH 0.08901907 0.11384295 0.15994524

SL 0.05726933 0.11921727 0.15071159

SN 0.05400855 0.10643512 0.10341280

ST 0.08821395 0.21120287 0.15280711

TH 0.08234046 0.13902924 0.17720208

The strongest specialization can be found in the city states Berlin (BE) and Hamburg (HH), while Niedersachsen (NI) and Nordrhein-Westfalen (NW) show the lowest values in all three indicators. As already mentioned in the concentration example, we have to remember the large-scale aggregation unit. If we used smaller scale units (e.g. counties like in Section 3.2.2), our results would surely be more differentiated. Again, we check the correlation between the indicators:

H j G j K j

H j 1.0000000 0.9179127 0.9322604

G j 0.9179127 1.0000000 0.7907841

K j 0.9322604 0.7907841 1.0000000

Again, we find a strong positive correlation between the Hoover coefficient and both Gini and Krugman coefficient (Hj vs. Gj: r ≈ 0.92, Hj vs. Kj: r ≈ 0.93), while the third Pearson correlation coefficient is a little lower, but still showing the same direction (Gj vs. Kj: r ≈ 0.79).

Now we check for clusters in a combination of a specific industry and a specific region. First, we calculate location quotients for the dataset G.regions.industries using the REAT function locq2(). Here, the optional function argument LQ.norm could be used for computing z-standardized location quotients according to O’Donoghue, Gleave (2004) (LQ.norm = "OG") or z-standardized values of the natural-logged LQs according to Tian (2013) (LQ.norm = "T"). However, we produce the original LQs, since we need exactly the same columns as in the examples above:

G.regions.industries$ind_code, G.regions.industries$region_code)

The output is a matrix with J rows and I columns:

I = 17 industries, J = 16 regions

BB BE BW BY HB HE

WZ08-B 2.5314363 0.04030901 0.6607950 0.8078054 0.0000000 0.3735773

WZ08-C 0.6857231 0.37224900 1.3968652 1.1902785 0.7863570 0.8580352

WZ08-D 1.1736475 0.46721079 1.0861988 0.8343784 0.9179718 0.9627955

WZ08-E 1.7945685 1.30128835 0.5896526 0.7137388 1.2393228 0.8532203

WZ08-F 1.5997778 0.77160121 0.9070096 1.0280409 0.6212923 0.8927681

WZ08-G 0.9550127 0.83133221 0.9492523 0.9879826 0.9013193 1.0006321

WZ08-H 1.3212794 0.87982228 0.8189666 0.8664163 1.7692815 1.2208728

WZ08-I 1.0379426 1.35561299 0.9132949 1.0390886 0.9904308 0.9571339

WZ08-J 0.5625876 1.78334039 1.0316114 1.1550764 1.0577107 1.1407078

WZ08-K 0.6529329 0.76630600 0.9329930 1.1058890 0.7825178 1.6710583

WZ08-L 1.1088846 2.13220960 0.7310014 0.8633894 1.3254723 1.1132939

WZ08-M 0.7366238 1.39880205 1.0337139 1.0265993 1.1202532 1.1457770

WZ08-N 1.2571301 1.24261162 0.7977054 0.8486971 1.2938161 1.0525912

WZ08-P 0.9052976 1.38842157 0.9649289 0.9252245 1.0563169 1.0085207

WZ08-Q 1.1540423 1.09329902 0.8695241 0.9079679 0.9544891 0.8980680

WZ08-R 1.0656945 2.55595102 0.8518192 0.8220540 1.3196613 0.8651451

WZ08-S 1.1409373 1.32596177 0.8626829 0.9092125 1.1396616 1.0528184

HH MV NI NW RP SH

WZ08-B 0.6029388 0.6235796 1.4987086 1.4595767 1.0371236 0.5078145

WZ08-C 0.4781934 0.6230156 0.9512438 0.9312325 1.0822678 0.7082513

WZ08-D 0.4332870 1.0118838 0.9932719 1.2139740 0.9349679 1.1248685

WZ08-E 1.1442005 1.5642257 1.0645497 1.0408356 0.9886860 1.0707585

WZ08-F 0.5432163 1.2716537 1.0969756 0.8735506 1.1134885 1.1043449

WZ08-G 1.0654315 0.9485377 1.0758977 1.0612190 1.0111274 1.2456100

WZ08-H 1.4958610 1.1243732 1.0409143 0.9961224 0.9633972 1.0112557

WZ08-I 1.0634066 1.7574637 1.0227196 0.8750205 1.1121264 1.2483966

WZ08-J 1.9266913 0.4751473 0.6716376 0.9830609 0.8122058 0.7496925

WZ08-K 1.5175078 0.5383900 0.9108456 1.0205798 0.8879292 0.8355178

WZ08-L 1.5871838 1.3034074 0.8040270 0.9928161 0.7774500 1.1980553

WZ08-M 1.6293913 0.6897571 0.8693026 1.0366589 0.7764558 0.7905498

WZ08-N 1.2530608 1.2484353 0.9675147 1.0659893 0.8026181 0.9727871

WZ08-P 0.9422739 0.9966228 1.0888054 0.9846351 1.0976178 0.9540262

WZ08-Q 0.8564604 1.2893168 1.0728412 1.0595648 1.0418460 1.1662290

WZ08-R 1.4914564 1.0500685 0.9204586 0.9611539 0.8498053 1.0418794

WZ08-S 0.8055128 1.1158184 0.9965451 1.0283571 1.1658852 1.1455178

SL SN ST TH

WZ08-B 0.2826284 1.2746172 2.4654331 0.7140637

WZ08-C 1.1752810 0.9867417 0.9297172 1.1849897

WZ08-D 1.1465539 1.0637093 1.2642787 0.8607578

WZ08-E 0.9555581 1.4457486 1.8251853 1.6042935

WZ08-F 0.9016858 1.3794286 1.4104724 1.3481005

WZ08-G 1.0370901 0.8787739 0.9172598 0.8661184

WZ08-H 0.8851047 1.0476688 1.2012430 0.8944907

WZ08-I 0.9111877 0.9496370 0.9020582 0.8644257

WZ08-J 0.7133587 0.7717704 0.4874344 0.6869177

WZ08-K 1.0082983 0.6620719 0.6133933 0.6316347

WZ08-L 0.7018816 1.1395422 1.0111694 0.8511896

WZ08-M 0.8060753 0.8459317 0.6627301 0.6814339

WZ08-N 1.0751749 1.1656467 1.2796548 1.1093251

WZ08-P 0.9147874 0.9658590 0.9798932 0.9710576

WZ08-Q 1.0760969 1.0475595 1.1401680 1.0628602

WZ08-R 0.7631263 1.1419135 0.8329295 0.8582919

WZ08-S 0.8840741 0.9774726 0.9257397 1.0923137

These I * J = 17 * 16 = 272 coefficients are too much information. Thus, we calculate them again using the optional argument LQ.output = "df", which produces a data frame with I * J rows and three columns (j_region: ID of region j, i_industry: ID of industry i and LQ: location quotient LQij). We save the results in the object lqs:

G.regions.industries$ind_code, G.regions.industries$region_code,

LQ.output = "df")

As we forego an inspection of these singe values, the results are not displayed here. Instead, we only deal with the five highest LQs in our results (the “top five”). We sort the resulting data frame decreasing and take a look at the first five rows:

# Sort decreasing by size of LQ

lqs_sort[1:5,]

j_region i_industry LQ

33 BE WZ08-R 2.555951

1 BB WZ08-B 2.531436

239 ST WZ08-B 2.465433

28 BE WZ08-L 2.132210

111 HH WZ08-J 1.926691

The highest LQ is found for the arts, entertainment, and recreation sector (WZ08-R) in the German capital Berlin. Note that this result is congruent with several studies about the “creative class”, showing a large stock of “creative” employment in Berlin (e.g. Martin 2015). We also find a strong concentration of mining and quarrying in two Eastern regions, Brandenburg and Sachsen-Anhalt. Note that the LQ is a relative measure with respect to the total regional employment as well as the total industry-specific employment and the employment in the whole economy, not considering other aspects of industry or spatial structure.

These deficiencies should be overcome with the Litzenberger-Sternberg cluster index, also taking into account area, population and firm size. This additional data is also included in our current dataset (columns area_sqkm, pop and firms). The functions litzenberger() and litzenberger2() work equivalently to locq() and locq2(). To compute cluster indices for all I * J combinations, we use the function litzenberger2():

G.regions.industries$ind_code, G.regions.industries$region_code,

G.regions.industries$area_sqkm, G.regions.industries$pop,

G.regions.industries$firms)

Like in locq2(), the default output is a matrix with I rows and J columns:

I = 17 industries, J = 16 regions

BB BE BW BY HB HE

WZ08-B 0.5736692 0.05611505 0.8041813 1.1073446 NaN 0.4745084

WZ08-C 0.1610679 3.24717820 2.6250805 1.2043415 5.119669 1.0603087

WZ08-D 0.2213627 1.37720778 1.7043505 1.4178208 4.172162 0.8541359

WZ08-E 0.8810260 10.14891585 0.8235517 0.6890213 6.705744 1.1427285

WZ08-F 0.7142888 11.36434353 1.2372108 0.9442221 3.498921 1.1225087

WZ08-G 0.2707787 12.10626625 1.3903532 0.9404677 7.136205 1.3361060

WZ08-H 0.4386878 13.26265081 1.0955747 0.7982074 22.656924 1.8358272

WZ08-I 0.2672336 26.60020727 1.4098657 0.9633029 8.481338 1.2880210

WZ08-J 0.1130326 59.24931837 1.4342037 1.2393579 8.683998 1.9024826

WZ08-K 0.1524825 10.28664194 1.4774980 1.1692461 6.650213 2.4739044

WZ08-L 0.2564814 56.65943460 0.9594093 0.8695636 11.839900 1.6099929

WZ08-M 0.1685895 39.30149403 1.5306799 1.0110472 9.410498 1.7302434

WZ08-N 0.4232166 26.91532975 1.0228326 0.7471872 10.796027 1.5265846

WZ08-P 0.2043023 25.30839556 1.3656409 0.9509028 7.322709 1.4627871

WZ08-Q 0.3445630 21.86956483 1.1770297 0.7873877 7.850886 1.2163624

WZ08-R 0.2450932 104.73565741 1.0839767 0.7821779 10.555369 1.0489672